You would be hard pressed to find anyone who followed economic news over the summer who did not hear about the inverted yield curve in American government bonds. It was one of the biggest and most significant topics of debate over the summer and, yet, the phrase ‘inverted yield curve’ is often greeted by mystery and quizzical looks, even among experienced amateur investors.

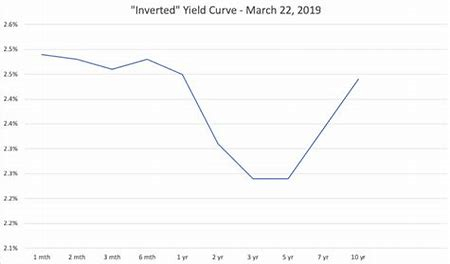

An inverted yield curve most commonly refers to a situation where the yield to maturity (YTM) on some government bonds with low residual maturity is higher than some bonds with high residual maturity. This means that the yield on shorter-term bonds (bonds with, say, 3-12 months left before expiration) is higher than that on longer-term bonds (bonds with, say, 5-10 years left before expiration). This is a very unusual situation. Normally, the yield curve is an upward sloping line, but, in an inverted yield curve situation, there will be a chink in the curve, as shown below:

The most commonly quoted yield spread is 10 year – 2 year spread. If this spread is negative (i.e. the yield on 10-year bonds is lower than that on the 2-year bonds), then there is an inversion. This is the inversion that investors really panic about, since it is often seen as a ‘predictor’ of a recession. To understand why this is true, we first need to understand why investors usually demand a higher yield on longer-term bonds. This is all to do with uncertainty. There is uncertainty about what inflation and monetary policy will be in the future – if inflation and interest rates go up in the future, then the value of your bond will go down and so, to account for this risk, you will buy long-term bonds only when they are offering a higher yield than short-term ones.

There is even economic uncertainty – namely that, for longer-term bonds, there is a higher risk that the government will not, in the future, be able to pay their debts, and that the default rate may increase. That longer-term bonds are a riskier investment than shorter-term bonds means investors demand a higher yield for the extra risk they are taking. In the situation of an inverted yield curve, these factors change around.

Yields on long-term bonds are lower than those on short-term ones because investors see it as more likely that inflation and interest rates will go down. This means investors might think consumer spending will decrease (leading to lower inflation) – which is a key cause of a recession – or that monetary policy will ease to order to stimulate the economy following a recession. Either way, both are linked to the occurrence of a recession.

Similarly, if investors fear a recession, they might want to buy up lots of long-term bonds to protect their portfolio from equity downturns over an extended period of time (long-term bonds thus become a safe-haven rather than riskier investment) and they might also feel that the government is more likely to default on shorter term debt, if the economy is in recession, than on longer term debt.

Finally, a prolonged inversion can lead to problems in the financial system, leading to a lack of inter-bank and bank-to-person lending, which can freeze the economy. This is because, as the saying goes, banks borrow money at short-term rates and lend at long-term rates. While this is an oversimplification, it does show that an inverted yield curve reduces the profitability of banks and their willingness to lend. In any cases, the increased buying of long-term bonds, which reduces their yield (since prices move inversely to yield), is a sign that investors are worried about a recession and its consequences. Indeed, an inverted yield curve, of this type, has preceded all of the last 11 recessions.

Thus, when the 2yr-10yr curve inverted in the middle of august, investors were understandably nervous about its potential significance. However, in my opinion, this inversion may be different to the last ones. This is largely due to the low-interest rate environment and easing monetary policy environment that is prevailing. In particular, a key macroeconomic trend of the last 6 months or so has been easing monetary policy across the globe (indeed the fed recently cut rates for the first time since 2008) and negative YTM on some European bonds. This has two key consequences.

Firstly, if investors are predicting easing monetary conditions over an extended period, then this sends the yield on longer-term bonds down, as discussed, even if the monetary policy is pre-emptive – especially in the US – and not because a recession is, in the opinion of central bankers such as Powell, around the corner. Secondly, the fact that there are negative rates in Europe means investors across the globe flock to long-term American bonds to lock up some kind of yield for the coming years, even if it is just 1.5-2%. This frantic buying of long-term American bonds, which is not because of recession fears, sends down their yield, thus inverting the curve.

Even if the inverted yield curve were stimulated by recession fears, there are still some technical reasons why we should not necessarily be expecting a recession. Firstly, the inversion was very short – lasting just a few days – and so it was not a prolonged, deep and emphatic inversion. Secondly, on average, it takes more than 12 months for an inverted yield curve to end up in a recession and it often takes more than two years. For example, before the 2008 recession, the yield curve first inverted in late 2005/ early 2006. Furthermore, not all of the last inversion resulted in a recession occurring at all. Indeed, in the months following an inversion, the equity markets are often positive – for example the S&P 500 averages a 1.5% return in the 6 months following an inversion and a 9.2% return in the 24 months following one. Thus, in the short term, an inversion may actually be a positive sign for investors.

In this way, while we should certainly stay on our toes regarding a recession – and there are plenty of other reasons, besides the inversion, why a recession might be imminent – there is no guarantee when, or even if, it will happen.