Since New Zealand’s adoption of an inflation targeting system to guide monetary policy in 1990, 25 other countries have followed suit. However, in the wake of the 2008 financial crisis, big-hitting economists such as Gregory Mankiw, Paul Krugman and Scott Sumner have proposed alternative methods, such as nominal GDP targeting and price-level targeting. The question the debate raises is two-fold: has inflation targeting brought prosperity, and if so, has it been preferable to other policies?

In order to answer the query set, we must first look at the definitions and parameters surrounding the practice. The main features of inflation targeting are: publicly announcing a numerical target inflation rate, either in the form of a range, or explicit point target, implementing policy which places emphasis on forecasted inflation, and manifesting a high degree of transparency and accountability in the outcomes of policy, if not the policy itself. The institutions which are associated with the policy tend to have a mandate for price stability, de facto independence from the government, and accountability for the central bank to the mandate. The generally accepted ‘optimal’ inflation rate is 2-3% among industrialised economies, which is thought to be close enough to zero to be plausibly defined as price stability, whilst maintaining a safe distance from deflation, which many argue might be worse than high inflation. Economic prosperity can broadly be measured by the rate of growth of real GDP, as well as levels of unemployment and levels of inflation.

A major benefit of inflation targeting is that it has created transparent central banks, and as a corollary, brought better policy with it. This can be seen in the Bank of England’s quarterly Inflation Report, which details the economic analysis and inflation forecasts that the Monetary Policy Committee uses to inform its interest rate decisions. The release of this easily comprehensible information to the public means that businesses are able to plan for future interest rates, thus leading to better informed choices. Furthermore, with these reports, central banks then have to detail the trade-offs they make in terms of unemployment and inflation, making these decisions more transparent. Thus, with the added measures of transparency, central banks are less likely to become inconsistent over time, leading to more effective policy. The impact of this system also means that central banks are less subject to institutional political pressure, as their mandate is more to the maintenance of stable prices and the growth of the economy rather than to an individual administration. The credibility gained from transparency in the short term grants flexibility in the long term, enabling better monetary policy.

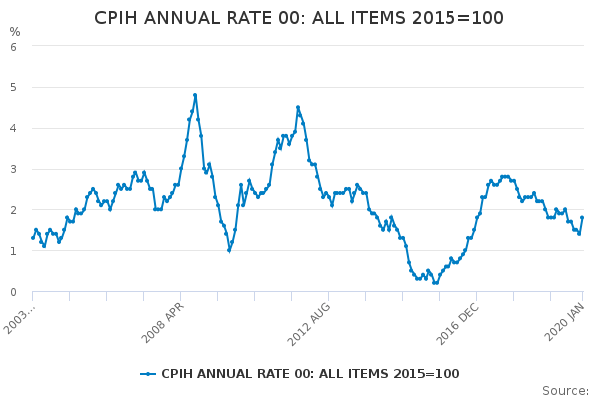

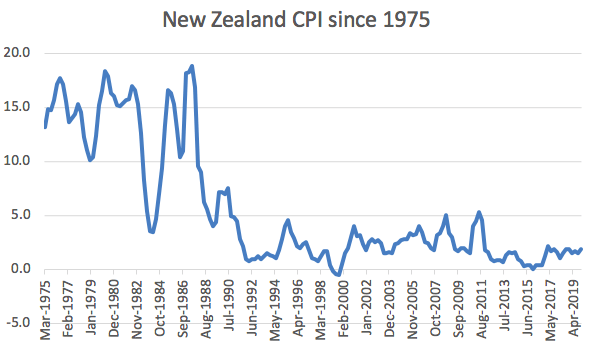

Another key aspect of inflation targeting is that it maintains price stability. Since the recovery after the 2008 financial crisis, the UK inflation rate has averaged at 1.7%, despite severe shocks to the economy in the form of Brexit. In fact, since the introduction of a 2% target in 2003, the CPIH, the UK’s inflation index, has pivoted mainly around the 2% point (see Figure 1), contrasted to average inflation rates of 6% in the three decades before. Furthermore, looking at New Zealand’s original implementation, the CPI has averaged at 2.1% since the start of the new policy, despite sizable fluctuation during the Great Recession (see Figure 2). It is clear that there is a trend towards lower rates of inflation following the implementation of inflation targeting in industrialised countries. Even in emerging market economies, where inflation targets tend to be higher, the countries which do implement it see success when it comes to providing price stability. For example, Chile, targeting a 3% inflation rate, has achieved an average of 2.9% for the past decade, compared around double that beforehand.

Figure 1 – The CPIH of the UK, 2003-present:

Figure 2 – the CPI of New Zealand, 1975-present:

The reason many institutions have placed such heavy emphasis on price stability is that it tends to lead toward economic growth and fewer unintended consequences. The transparency added when inflation targeting is properly implemented reduces investor uncertainty significantly over time. Moreover, if inflation happens at a high rate, consumers tend to lose purchasing power and see their savings wiped out, which has detrimental effects, most clearly seen in extreme cases of hyperinflation, such as in Weimar Germany or Brazil in the 1980s, where prices rise and existing assets decrease in value. However, deflation can be equally harmful, as falling prices lead to a slow-down in growth, mostly due to the incentive to delay spending as goods and services become cheaper. In developed countries, as shown in a 1997 study of four countries (New Zealand, Canada, the UK, and Germany), growth has been consistent and unemployment low. The UK’s unemployment rate since the financial crisis has averaged at 5.1% contrasted to the 7.8% average before inflation targeting was implemented.

It is quite clear that inflation targeting has largely been successful in delivering price stability with growth in recent years However, it is necessary to compare it to other methods which have been suggested. There are two main contending alternatives. The idea of NGDP targeting, i.e. targeting the growth of the economy as a whole, not accounting for inflation, gained momentum in the post-financial crisis recession and it is still popular today.. The main argument some economists have used is that NGDP targeting is able to deal with both supply and demand side shocks. This is because both inflation and NGDP targeting would suggest similar reactions to demand side shocks. However, in a supply side shock, inflation targeting would imply a tighter policy than is NGDP targeting, the damaging consequences of which were seen in the 1970s oil crisis.

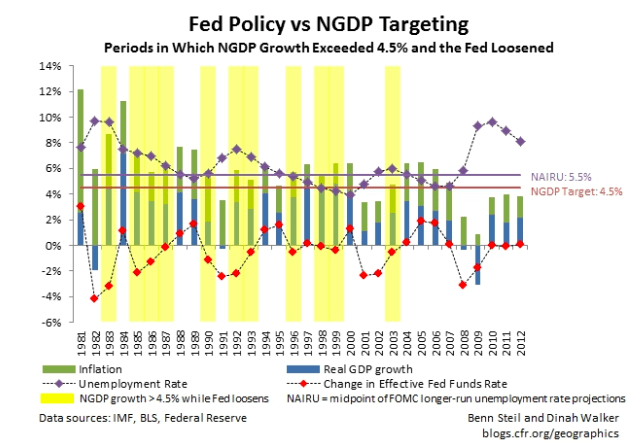

More recently, some people argue that it would have called for looser, more aggressive policy during the financial crisis. There are two responses to this practice. First, in practice, the correlation between inflation and NGDP is too tenuous to maintain the price stability necessary to sustain economic growth. Second, there have been 11 years since 1980 in which the Fed advocated for loosening, whilst NGDP growth was above 4.5%, the target most proponents of nominal income targeting deem ideal (see Figure 3). Thus, this method may work in developing economies, where supply side shocks are more frequent, but is not a viable solution in general, a view shared by Mishkin and Woodford in the Wall Street Journal.

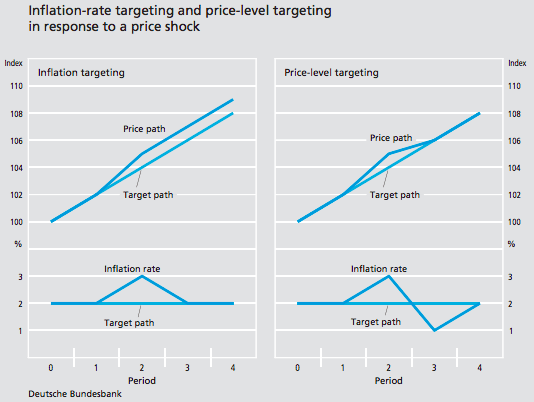

Another alternative practice is price-level targeting, which differs from inflation targeting mostly in its response to economic shocks. Whereas inflation targeting treats them as bygones, price-level targeting corrects for any changes in the system to revert the price level back to its initial trend. This has the theoretical benefit of being able to better respond to deflationary shocks at the zero-lower bound because there would be a credible expectation that future inflation would be above trend. The benefit is that price levels would not be impacted as much by supply shocks (see Figure 4). However, a price level target would also force central banks to correct for supply side inflationary shocks, with unnecessary adverse effects (see Figure 4). Furthermore, it has traditionally been perceived that there would be a trade-off between long-term stability and short-term fluctuations. There is still much debate on both sides of the argument, as price-level targeting could have better impacts than the status quo, but remains untested and purely theoretical.

Figure 3 – Fed Policy vs NGDP Targeting (Areas marked in yellow are periods during which Fed Policy loosened, but NGDP Targeting would have recommended tightening):

Figure 4 – Comparison of inflation targeting and price-level targeting in response to supply shocks:

Overall, inflation targeting is not a perfect system, as it has imperfections in theory and it cannot be applied to all economies. However, it must be said that there are tangible benefits associated with the adoption of the system, ranging from price stability to economic growth. The current implementation has also led to a successful recovery from the recession after the 2008 financial crisis. The most commonly toted alternatives cannot be said to be preferable over the long-term, and their application is restricted largely by their theoretical nature. Therefore, future uncertainty notwithstanding, it is clear that inflation targeting has had a positive impact on the economic prosperity of countries which have implemented it.