As a barometer of society’s civilisation, the UK’s care home sector is important. However, employing more people than the NHS, it is economically and politically important too. Clear and visible demographic change is set to dramatically accentuate the pressures on the sector, and the political choices we are forced to make as a result will define our society. So, what will the boomer generation do?

As a sector, residential care for the elderly is worth around £16 billion a year in the UK, catering for around 410,000 residents. Around 51% pay for the full cost of their care, an estimated £846 per week (£44,000 per year), while local authorities (LAs) provide funding for the other 49%, representing £6.5 billion of their £100 billion annual budget.

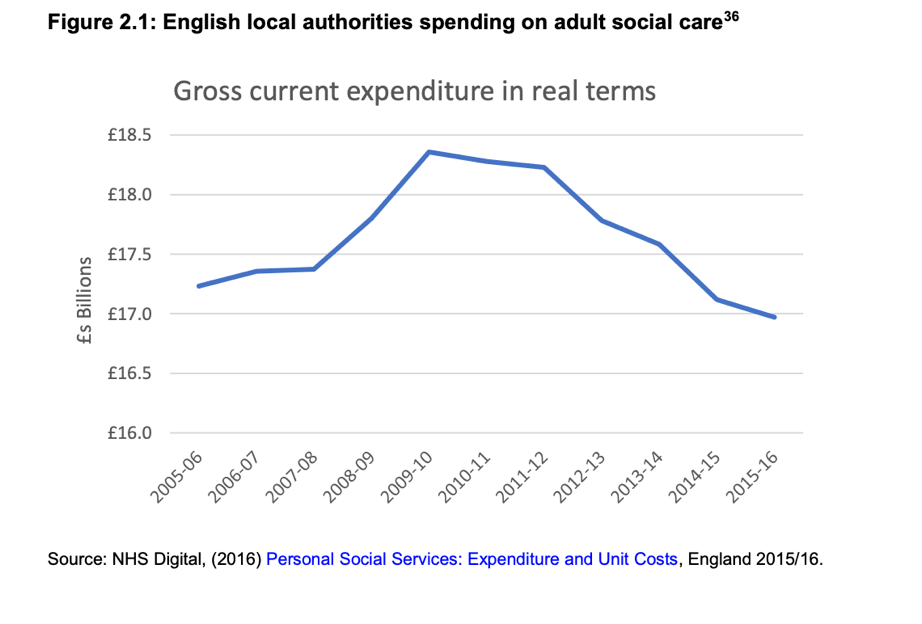

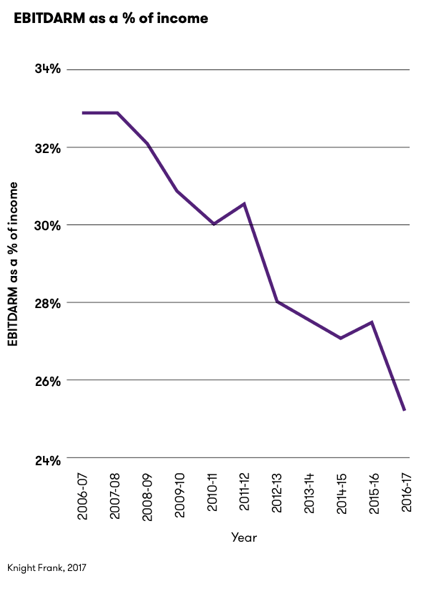

But austerity measures post the global financial crisis have put pressure on LA budgets and they have responded accordingly – as the reduction in expenditure on adult social care (residential and at home) in figure 1 below shows. Reduced care home fees, despite escalating labour, food and property costs, have massively reduced operator profitability as demonstrated in figure 2.

Source: https://assets.publishing.service.gov.uk/media/5a1fdf30e5274a750b82533a/care-homes-market-study-final-report.pdf

Source: https://www.grantthornton.co.uk/globalassets/1.-member-firms/united-kingdom/pdf/documents/care-homes-for-the-elderly-where-are-we-now.pdf

To remain viable care homes rely on charging self-funders 40% more than their LA funded counterparts. Homes with a high percentage of LA-funded patients are in an unenviable position, struggling to meet day-to-day costs and unable to cover additional investment costs. Without the financial backing to modernise facilities only two outcomes are inevitable; closure or exiting the LA-funded segment of the market. This situation pertains to roughly a quarter of the 11,300 care homes in the UK.

The truth of the matter is serving LA-funded residents has become undesirable. Only 5% of all UK care homes run on a not-for-profit basis – the rest are run as investments to generate a return. As illustrated in figure 3 below, financial incentives for filling a home with mostly LA residents are low – with 15% less profit than if it were filled with self-funding residents.

Source: https://assets.publishing.service.gov.uk/media/5a1fdf30e5274a750b82533a/care-homes-market-study-final-report.pdf

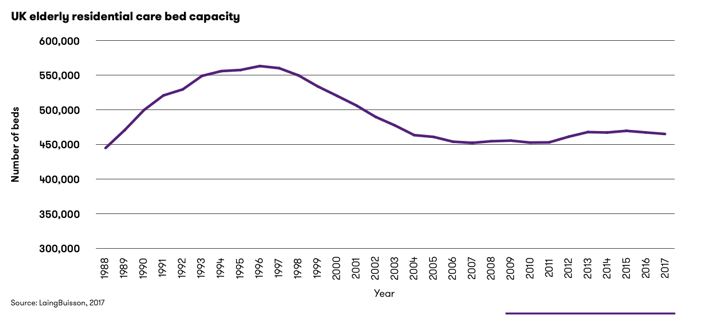

In figure 4 we can see the effect that this has had on the industry. In the 10-year period between 1996 and 2006 over 100,000 elderly residential care beds were lost. Many care homes which catered for primarily LA-funded residents had to close as they were no longer financially viable. Since 2006 the overall number has remained stable as new self-funded home capacity offset these closures. But this capacity is only built in areas that can sustain self-funder demand causing major supply issues in LA dependent regions.

Source: https://www.grantthornton.co.uk/globalassets/1.-member-firms/united-kingdom/pdf/documents/care-homes-for-the-elderly-where-are-we-now.pdf

So, the care home market is already under pressure today, but what are its prospects in years to come?

Source: https://www.grantthornton.co.uk/globalassets/1.-member-firms/united-kingdom/pdf/documents/care-homes-for-the-elderly-where-are-we-now.pdf

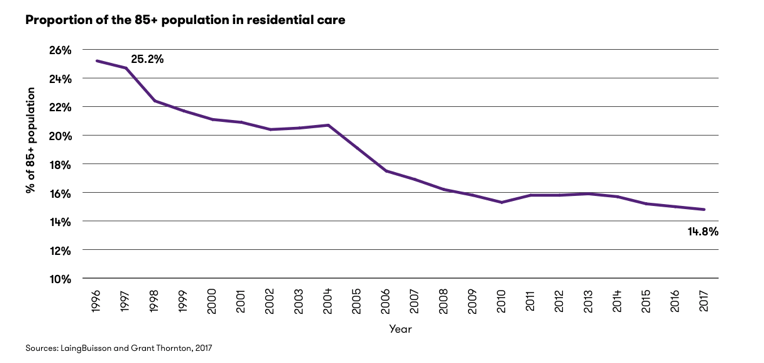

Figure 5 above shows the UK’s ageing population demographic. The Office for National Statistics predicts a 36% growth in persons aged 85+ from 1.5 to 2 million by 2025 and then to 2.8 million by 2031 an increase of c.75%. This is not a new phenomenon. There has been an increase of more than 45% in this demographic since 2001 but, as figure 6 shows, this hasn’t translated into increased demand for nursing home beds. Instead, demand as a proportion of the relevant population has fallen by 4.4% from 2001-2016.

Source: https://www.grantthornton.co.uk/globalassets/1.-member-firms/united-kingdom/pdf/documents/care-homes-for-the-elderly-where-are-we-now.pdf

So why didn’t the demographics boost nursing home demand? The explanation lies in the behaviour of LAs. In response to escalating demand and budgetary pressures, they increased eligibility criteria for residents and reduced referrals. This tightening, outlined in figure 6, cannot continue indefinitely for two reasons:

- The proportion of the over 85 population in care homes cannot continue to decline as it has done; and

- The rate of increase in the 85+ demographic is set to accelerate exponentially over the next 15 years.

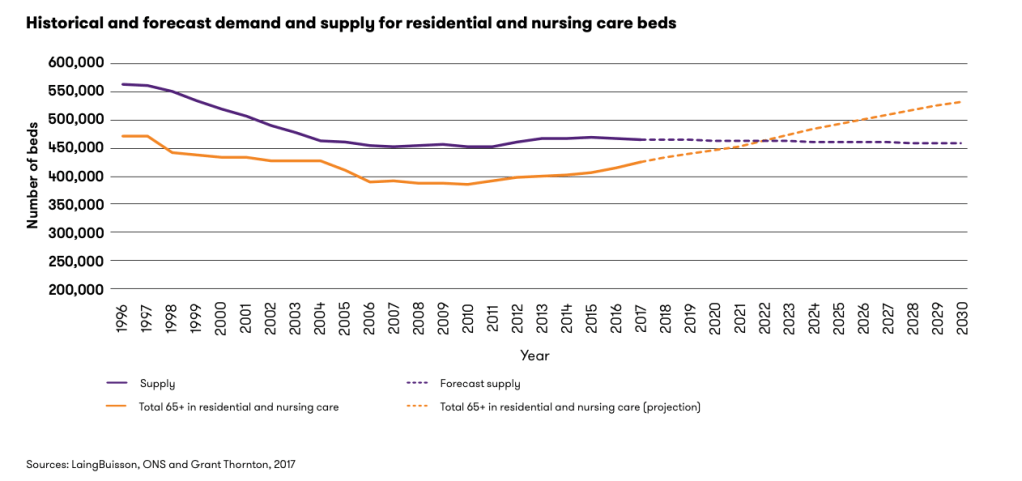

From 2008-2017 the rate of decline fell to 0.15% from averaging 0.75% each year for the previous 15. This has resulted in more pressure on operators facing increased acuity of clients who require more intensive care which is a large additional cost. As the proportion is now stabilising, the absolute population of over 85s is forecast to grow at a faster rate. Since 2004 it has grown by 40% (c479,000) and over the next 13 years is expected to grow by 62.6% (1,000,000+). This dramatic increase in demand will likewise require a large corresponding increase in bed supply which has otherwise been broadly stable with a very marginal decline (figure 4, 7).

Source: https://www.grantthornton.co.uk/globalassets/1.-member-firms/united-kingdom/pdf/documents/care-homes-for-the-elderly-where-are-we-now.pdf

Based on this escalating demand and contracting supply, recent projections by Grant Thornton have estimated the need for an extra 75,000 beds by 2030 and that the inflexion point of demand outstripping supply occurs now. Against this, LAs’ ability to meet any increase in costs is limited (see figure 7). What does this mean? A care home model that relies on LA support is unsustainable. If LAs want the private sector to build and operate care homes to meet this demand, they are going to have to offset the rising food, property and care costs by increasing the fees they pay per resident. Based on maintaining the current system of eligibility, spending will need to increase by 40% from 1.1% of GDP in 2018/19 to 1.5% by 2033/34 (all estimates are pre Covid-19). This funding gap is expected to have to be met by an increase in general taxation and has become a major political hot potato.

Just to sustain the current non-functioning market requires an increase in funding of £6.1bn by 2030 – additional measures to address the sources of dysfunctionality (for example to realign fees with underlying costs and meet escalating care needs) increase the funding gap to £14.6bn. This is equivalent to more than doubling the annual LA funding requirement. This cannot be achieved without a major increase in their funding from general taxation – requiring a 2.5% increase in income tax across the board. Meeting the demographic growth for the ten years thereafter is likely to see this increase double to 5%. No government wants to pay the political cost of defusing this timebomb when the alternative is to kick the can down the road and make it the next government’s problem.

I’m sure some people might find this a bit interesting.

LikeLiked by 1 person

Fascinating article, a great read

LikeLiked by 1 person

Some of these stats are remarkable!

LikeLiked by 1 person