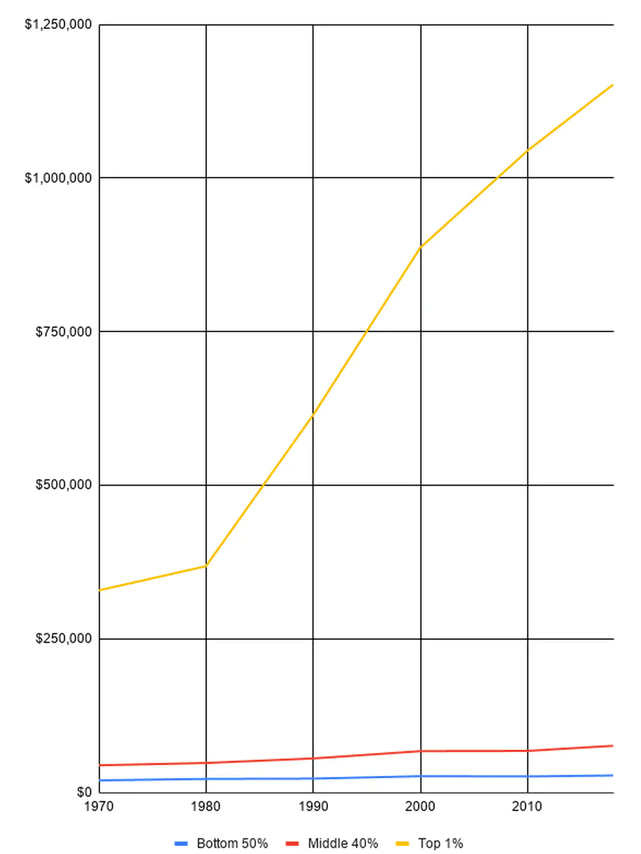

Source: https://www.commondreams.org/news/2019/12/09/staggering-new-data-shows-income-top-1-has-grown-100-times-faster-bottom-50-1970

26 billionaires own as much as the world’s poorest 3.8 billion people – perhaps unsurprising given how little the poor in developing countries own. Inequality is widely accepted as not only inevitable but desirable to an extent, to incentivise innovation and productivity, but in OECD countries it is at the highest level for the past half century. Those at the top of the income and wealth distribution have seen disproportionately higher gains while those at the bottom and even in the middle are actually worse off today than at the turn of the century, resulting in a hollowing of the middle class. Is the system rigged? I will address rent-seeking as a contributor to rising economic inequality experienced by the developed world of late.

What is rent seeking?

Rent-seeking involves increasing one’s share of existing wealth without creating new wealth. Adam Smith categorised income into wages, profit and rent. Wages are earned from employment (therefore producing a good or service) and profits are earned at the risk of capital(firms gain a return on selling a good or service for greater than the cost of revenue; investors lend to earn interest from bonds or provide capital to companies issuing stock expecting capital gains or dividends). “Rent” is commonly known as the payment from a tenant to a landlord for the use of a property, but evolved to mean receiving a payment exceeding the costs involved in the resource, e.g. through ownership of the resource. As rents do not create value, they redistribute income from the majority to the rent seekers and increase inequality.

Monopoly rents

Supernormal profits should not be possible under normal circumstances as competition prevents firms from charging a price significantly higher than the marginal cost of producing the product or they risk losing customers to competing firms charging less. Monopolies can restrict output below equilibrium to artificially inflate prices and extract consumer surplus.

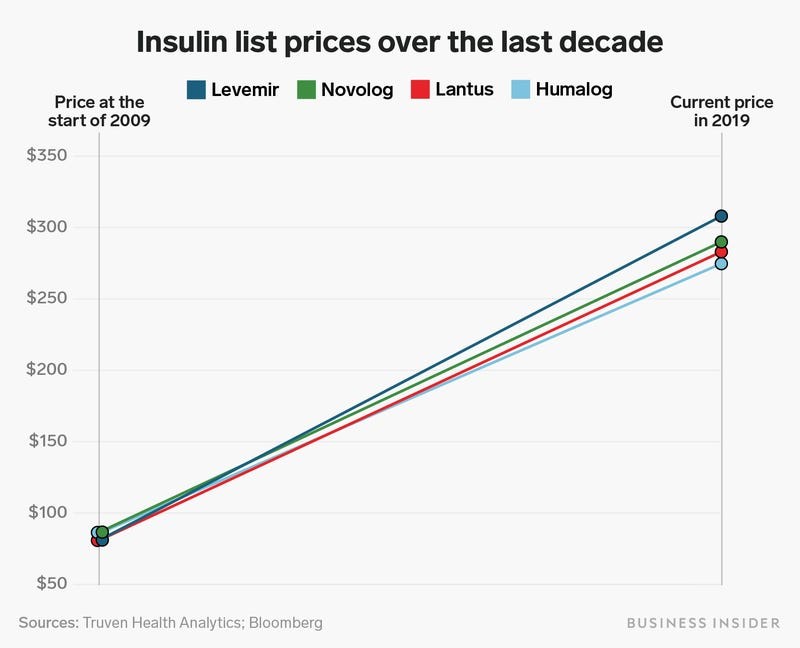

The pharmaceutical industry is a notorious example. Three pharmaceutical giants – Eli Lilly, Sanofi and Novo Nordisk – control 90% of the global insulin market. Their products Humalog, Lantos and Levemir have increased in prices by 1124% over 20 years, 614% over 15 years and 302% over 10 years respectively.

Insulin has a highly inelastic demand as type 1 diabetics require it to survive. The monopoly on insulin allows prices to be raised without risk of competition. Pharmaceutical companies justify their exorbitant prices by arguing that their R&D costs are huge because most drugs are ineffective, unprofitable or both. However, they do not mention that they spend twice the cost of R&D on sales and marketing – especially in the US where TV advertising is allowed – or that the rest of their cash flow goes to M&A, share buybacks and lobbying for tax breaks and public funding.

Monopolies can engage in predatory schemes other than inflating prices. Pay-for-delay schemes allow a patent holder to pay another company not to enter the market. Patents are intended to reward invention and innovation but had the unintended consequence of incentivising pre-emptive mergers to buy cheap potential competitors with promising or profitable drugs before they become a competitive threat, instead of carrying out their own R&D.

While almost a quarter of American patients have difficulty affording their prescriptions and two-thirds of Americans filing for bankruptcy do so due to medical bills, the pharmaceutical industry generates higher profit margins than any other (even higher than the banks!). From 2000-2018, 35 pharmaceutical companies reported combined net income of $1.9 trillion.

Regulatory capture

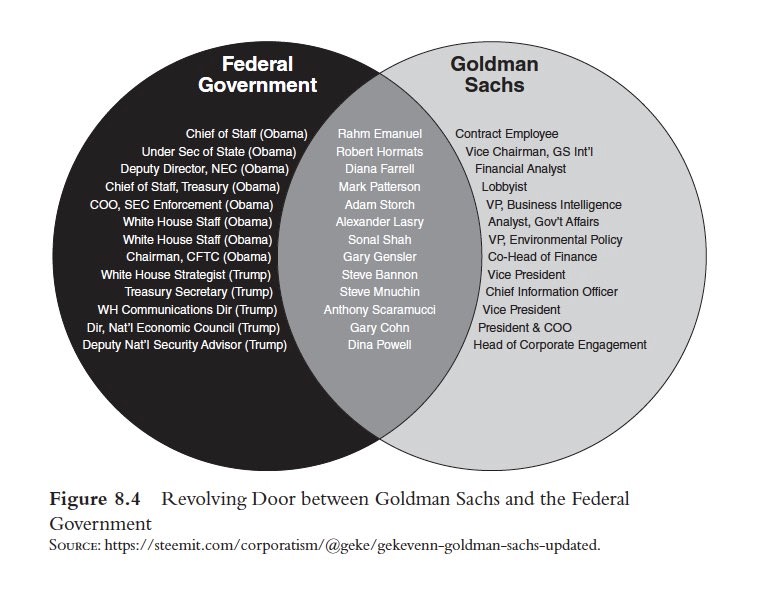

Regulatory capture is a form of rent-seeking where there is collusion between firms and the regulatory agencies intended to govern them. Usually those appointed to the regulatory agencies are industry experts to ensure the regulators understand the complexities of the industry, e.g. financial services. This is problematic: regulators’ incentives are aligned to those of the industry (often in conflict with those of society) and such regulators are then rewarded as they return to the industry after their government service. The industry captures agencies by vetoing any nominees whose sympathies do not lie with them. It defeats the purpose of a regulator if the industry regulates the regulator, who acts in private, and not in public interest. The banking industry had 2.5 lobbyists for every US representative, outspending even the healthcare sector, diluting any impact that the ‘Occupy Wall Street’ movement had. Outmatched in funding and fighting vested interests, ordinary citizens have limited influence on policy change even if they are the majority – a hard pill to swallow for citizens living in democracies.

Source: https://steemit.com/corporatism/@geke/gekevenn-goldman-sachs-updated

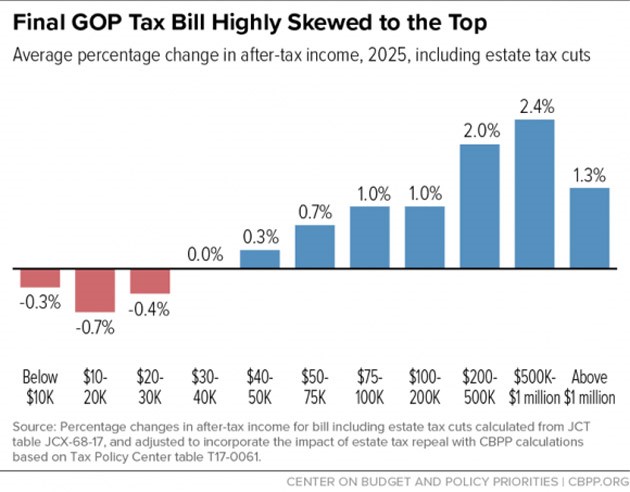

Buying lower tax rates – trickle-down economics

Rich taxpayers have been rewarded by policies based on trickle-down economics. The theory states that tax breaks and benefits for corporations and the wealthy will trickle down so everyone benefits. Firms use the extra cash for business investment such as buying a new factory and upgrading technology (boosting productivity and maximum output) as well as hiring new workers (creating jobs); and wealthy individuals spend more, creating demand for goods and services, leading to economic growth, which pays back the lost tax revenue. In practice, tax cuts for corporations often go to stock buybacks, benefiting shareholders – i.e. the wealthy – but not workers or consumers. Indeed, airlines have spent 96% of their cash flow on buybacks over the past 10 years. Wealthy individuals generally have a higher marginal propensity to save than the average citizen – only so many watches and cars they want to buy! Instead they are more likely to reinvest in assets, leading to further capital gains and investment income, and further wealth inequality.

Source: https://www.motherjones.com/politics/2017/12/what-will-trump-tax-bill-do/

Concluding remarks

I have mentioned some of the more nefarious causes of the disproportionate success of the wealthy but rising inequality is also the result of more benign changes that have disadvantaged the poor – namely globalisation and technological advances, which have reduced the demand for (and thus the earnings) of low skilled workers. Most importantly, inequality is reaching unacceptable levels and rent-seeking cannot be allowed to continue lest we descend into social breakdown and revolution.