Millions unemployed. The world in shock. Governments panicking. Both the financial crisis and the coronavirus pandemic left the globe reeling. Yet governments responded with their own bailout packages, their own furlough schemes and their own targeted welfare programs. It’s quite interesting how differently the public has reacted to these plans and in turn, how effective they were to actually solve both the short and long-term issues that that both crises brought.

We should start by comparing the monetary responses to the two crises. During the financial crisis, many central banks eased monetary policy aggressively in order to alleviate financial market distress, boost output and spending, and stabilize inflation. The methods used in 2008 largely consisted of slashing interest rates, round(s) of quantitative easing and targeted assistance to financial institutions such as banks. For example, by mid-December 2008 the Federal Funds Rate had reached nearly 0% and could go no lower. Consequently, the Fed encouraged Congress to pass the Troubled Asset Relief Program (TARP), a major bailout of the financial system. The bailout package cost $700 billion, but took two rounds of voting in congress to get through and faced major public backlash. This also gave companies like Morgan Stanley and Goldman Sachs access to cheap overnight lending. Finally, the US, in its first round of QE, bought $100 billion in agency debt and a further $500 billion in mortgage backed securities, growing its balance sheet immensely.

This trend of bailouts and QE has continued up until, and including, the coronavirus pandemic. Interest rates, however, have stayed surprisingly low, with the ECB interest rate staying at 0% since 2016, which gives central banks limited scope to cut interest rates as an effective monetary solution. Another crucial difference is that now, financial institutions are not the ones that need to be rescued, but rather companies and sectors that are impacted by lockdown (i.e. aviation). The Federal Reserve did two things this time round to prevent market losses. First, they cut interest rates to zero to encourage cost-free borrowing (although interest rates were already low to begin with). This was followed by a cast-iron guarantee to back Wall Street – hence the markets keep rising because they feel as though the bottomless pit of taxpayer money underwrites the risk that they face. The CARES Act allotted over $450 billion to fund asset purchases of $4 trillion. At the rate at which the Federal Reserve is buying, its asset-holdings may shortly equal $10 trillion – almost half the total US annual economic output. This time round, governments had very little scope to change interest rates, and so QE and bailout packages have drastically increased. In 2008, the Treasury knew the US public had no appetite for a bailout package of more than $1 trillion. Now, President Trump is asking for a bailout package that could well exceed $4 trillion, and the public have not objected.

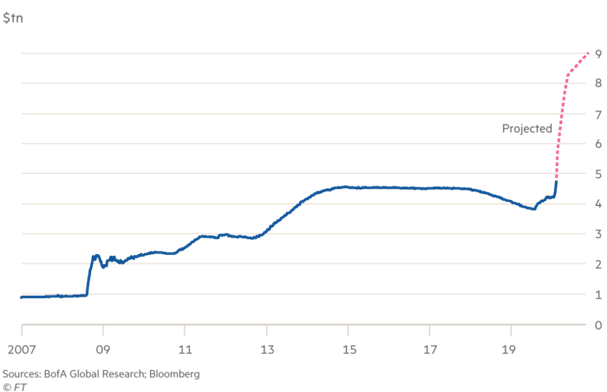

This graph illustrates the balance sheet of the US Federal Reserve since 2008. The first rise at 2008 was in response to financial crisis, and the second projected rise is in response to the coronavirus pandemic. There are two interesting things to note: firstly, the balance sheet only kept increasing since 2008, and secondly, the projected increase for 2020 is much higher than the increase in 2008, illustrating the loosening of monetary policy in the last 15 years.

There are both similarities and differences for fiscal policy as well. The Economic Stimulus Act of 2008 was a $152 billion package that consisted of a $600 tax rebate for low and middle income families in the US. This was presented as a cheque, signed by George W. Bush, that individuals could then spend immediately. Families were given $1200. Multiple schemes also took place in the UK. Throughout 2008, a number of measures were introduced including a £145 tax cut for basic rate tax payers, a temporary 2.5% cut in VAT, £3 billion worth of investment spending brought forward from 2010 and a variety of other measures such as a £20 billion Small Enterprise Loan Guarantee Scheme. The total cost of these measures, mostly announced in the November 2008 Pre-Budget Report was roughly £20 billion. Fiscal policy is most effective in a deep recession where monetary policy is insufficient to boost demand. Higher government spending will not cause crowding out because the private sector saving has increased substantially. Thus, by putting money into individuals’ pockets, governments are able to increase the spending and demand necessary to keep companies afloat.

The fiscal response to the coronavirus pandemic is largely similar. In the US, $600 billion has been allocated to direct payments of $1,200 to Americans earning up to $75,000. There is also the Paycheck Protection Program, which is $349 billion in federally guaranteed loans to small businesses. The loans carry interest rates of just 1 per cent and can be forgiven if companies do not fire workers. The UK’s fiscal response has been more interesting. They have allocated £42.0 billion for the Coronavirus job retention scheme, which is the furlough scheme that has dominated headlines. This is different to what we saw in 2008, and perhaps the UK has learned from its mistakes, because now instead of giving individuals money up front to use all at once, the money is spread out like a normal wage. This achieves two benefits: it prevents people from becoming unemployed, and it gives individuals a steady stream of money to spend. In 2008, both the fiscal and monetary responses were not able to curb unemployment, but a furlough scheme to supplement salaries (and keep jobs) is a targeted fiscal response that achieves this very aim.

Despite the fact that both these economic crises had two very different origins, some of the responses to tackle them have been strikingly similar. Ultimately, it is a combination of both fiscal and monetary responses that are required to deal with a crisis. While both monetary and fiscal policy has loosened since 2008, we saw a reversal of the fiscal policy in 2010 which led to the austerity in the UK – something that plagued the country for the best part of a decade. Will that happen again?