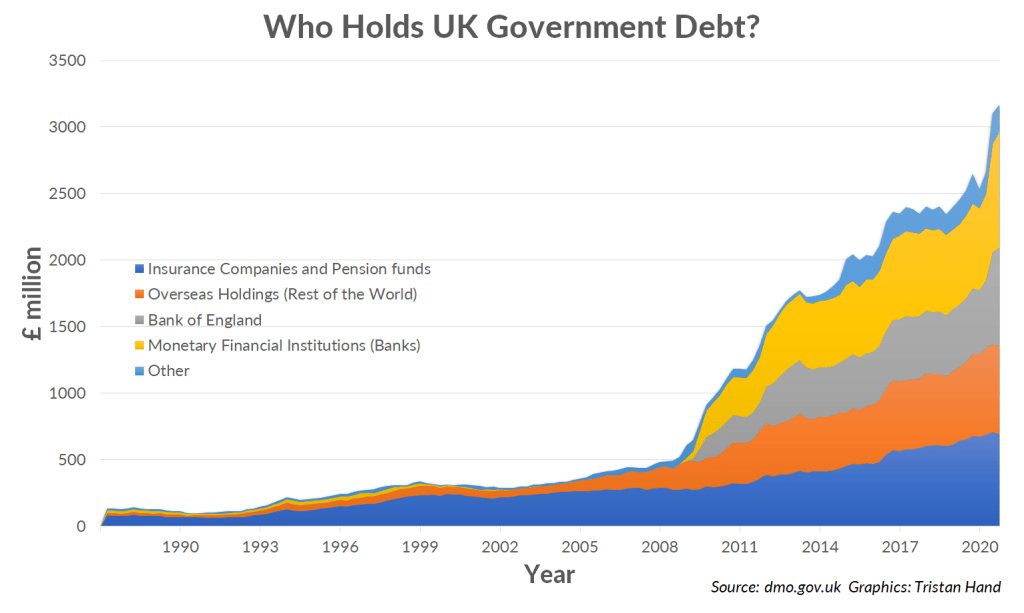

This Chart of the Month shows who holds UK government debt.

What is striking here is the increase in total debt after the 2008 financial crisis, as well as subtle changes to its ownership.

Significantly, the total value of bonds held by the Bank of England (BoE) has increased from £0 to almost £895 billion, worth 25% of total government debt. This is due to the introduction of quantitative easing since the 2008 financial crisis, a monetary policy response to insufficient aggregate demand.

To boost the economy, the BoE prints more money. This allows the BoE to repurchase large quantities of government bonds from banks and institutional investors. After selling their bonds, banks now have a surplus of currency in their accounts. They can reinvest this money by lending it out to more people. This increases the supply of loanable funds (making it easier to borrow), which encourages spending.

Like all borrowers, the UK government pays a set rate of interest to bond holders, known as the coupon payment. This is the cost of borrowing. The government will repay the entirely of the loan after a fixed period of time, known as the maturity. These timescales may vary from a few months to 50 years. However, interest is usually paid every year.

For instance, if the government issues a “£100 10-year bond, coupon payment 1%,” it is effectively saying: “Let me borrow £100 from you for 10 years. Each year I’ll pay you £1 worth of interest. After 10 years, I’ll repay the £100.”

Bond holders can sell their bonds before they are repaid by the government. The coupon payment as a proportion of this new price is the current bond yield. When prices are high, bond yields fall; when prices are low, bond yields rise.

For instance, consider our £100 10-year bond, coupon payment 1%. Suppose you buy that bond: your yield would be 1%. If I immediately buy that bond for £105, I only will be repaid £100 from the government, plus £1 paid each year for 10 years. My expected return is £110 – £105 = £5. Each year this is £0.50: the bond yield has fallen to 0.5%.

The repurchase of bonds by the BoE drives up prices, leading to a fall in bond yields. Now, if the government wishes to borrow, it can offer a much smaller coupon payment. The UK government knows it can always find a buyer for its debt.

Low bond yields reduced the cost of government borrowing to historically low levels. Any increases in government debt are not necessarily a cause for concern, as long as a large proportion of it remains with the Bank of England. This helps to keep the bond yield low and stop debt repayments from overwhelming government finances.

However, this has also made UK bonds less attractive to risk-taking investors who seek higher returns. This may explain why the proportion of debt held by insurance companies or pension funds has decreased in the past decade.

Recent shocks to the UK economy have had dramatic effects on the ownership of UK government bonds. With debt at an all-time high, we are only beginning to adapt to a new normal.

We leave you with today’s Question of the Month:

“How might the ownership of UK debt change in the future, and what economic effects might this have?”

Written by Tristan Hand and Chenyang Li

This Chart of the Month has been subsequently amended. The y-axis label of the chart has been changed to “£ million,” following clarification from the ONS. Special thanks go to Emily Knock for her assistance.

Data Sources

UK Debt Management Office (2021). Retrieved 2021-03-29.

Interesting chart, but could you clarify the y axis? What does thousands of bonds mean?

LikeLiked by 1 person

Thanks for pointing this out – I’ve got in touch with the ONS to clarify but have received no response as of yet. I’ll let you know as soon as possible once they’ve replied.

LikeLike

The ONS has confirmed that the units of the data series should be in £ million, not “thousands of bonds.” We’ve now changed the article to reflect this.

I sincerely apologise for our belated response on behalf of the editing team: we raised the issue a while ago but completely forgot to follow up. We’ll get back to future comments much sooner.

LikeLike

Great. Thanks for the clarification.

DJF

LikeLike