How happy would you be if I said you won £1,000? Presumably rather elated; but would you be twice as happy if I’d instead told you that you’d won £2,000? To most people the answer is almost immediate: “Well I’d be happier but probably not twice as much!” Likewise, most people would choose a guaranteed £1,000 prize rather than a 50% chance of a £2,001 prize, despite the expected value of the second option being greater. This is the foundation of Prospect Theory, which describes how different gains and losses affect our happiness; and, thought experiments aside, can have practical implications such as influencing how much we pay into our pensions.

Ever since their origins, economic models worked on the simple assumption that humans have diminishing marginal utility of wealth. This means that as one’s wealth increases, so does their happiness but at a decreasing rate. Whilst this gets the basic psychology right, its weakness lies in that humans notice changes far more than objective levels.

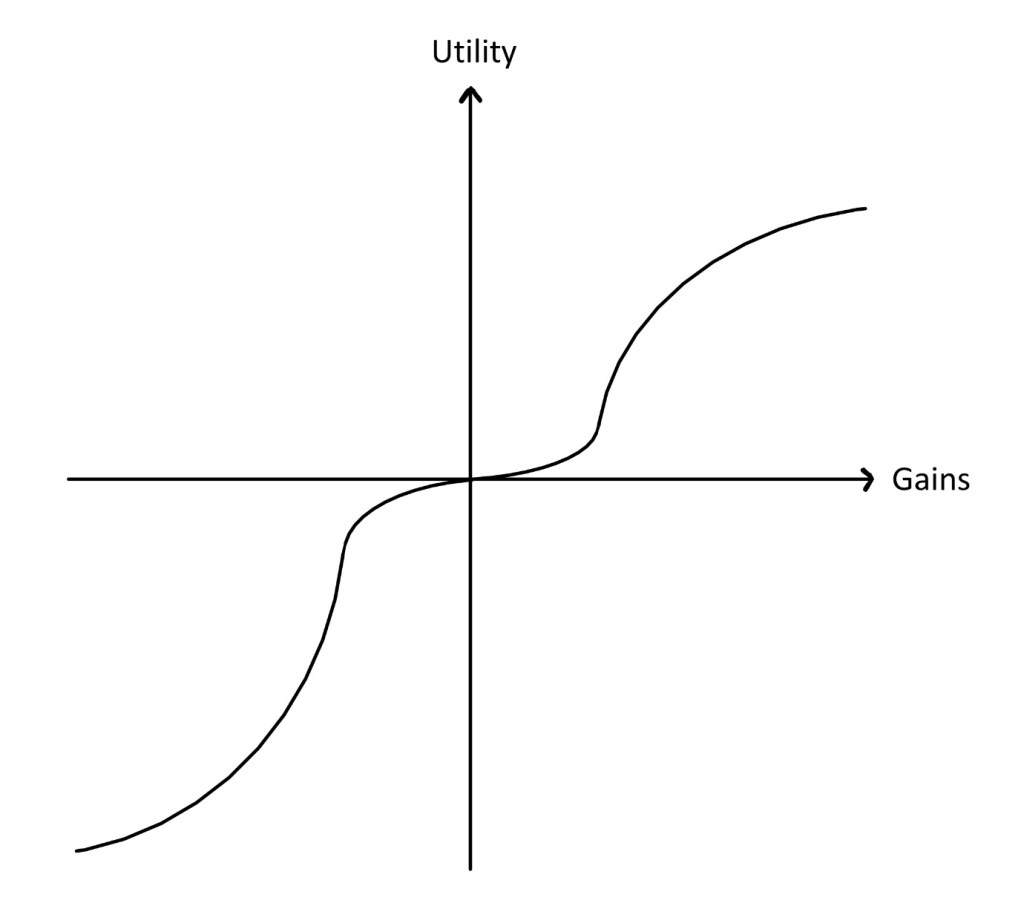

Here, Prospect Theory steps in. It describes a value function where the change in utility after receiving the first £1,000 is less than the second and so on. Whilst this concept, known as diminishing sensitivity, may seem obvious, it is crucial in understanding the leading drivers of human decision-making: risk aversion and loss aversion. Because of this diminishing marginal utility, humans are less likely to accept a chance of a higher windfall when there is the certainty of a smaller one on offer. The larger gain will give slightly greater utility than the smaller one, but the chance of nothing means that many are inclined to take the guaranteed option. This can be best demonstrated by the graph below, which shows utility increasing as gains do but at a slowing rate.

What is also fascinating here is the opposite side which shows how we tend to respond to losses. At first it can look like a mirror copy, increasing losses cause more pain but at a diminishing rate. However, the key part is the far steeper rate of the line, suggesting that humans experience more pain from a loss than they would happiness for a similar gain. This phenomenon called loss aversion means that we are disproportionately fearful of losses and their consequences. The biological explanation of this can be traced to the very evolution of the human race.

In primitive environments it was beneficial for humans to be loss averse since any small misfortune such as an injury would not only endanger oneself, but also one’s offspring and community that had to care for them. A series of losses may have quickly resulted in death due to the limitations of healthcare or social support structures, whereas a series of gains would have, at best, meant that the group were better fed and healthier. This caused humans (and other animals) to adapt a disproportionate fear of losses and an instinct to avoid them at all costs.

This manifests itself in the characteristic of taking risks to avoid a loss. As the opposite of our risk aversion to gain, people tend to prefer a chance of avoiding losses (say a 90% chance of losing £1,000) to a smaller guaranteed one (£899) even if the expected outcome is worse (£900 vs £899). The larger loss will result in slightly more pain than the smaller one, but the chance of avoiding it makes it more appealing.

People are also irrational when it comes to lotteries and gambling. The expected value of a lottery ticket is always less than the ticket itself since the companies that run them need to make money. However, contrary to Prospect Theory, a majority of people, if offered a lottery ticket or its monetary value, will choose the ticket. There are two main reasons why someone might turn down the small certain gain and choose a small chance of a large win. The first is the fact that humans are bad at estimating probabilities and tend to overestimate the tiny chance (1 in 45 million) that they might win, therefore incorrectly calculating the expected utility (utility if won * chance of winning). The second is that the Prospect Theory graph is inaccurate, and a better model is the Markowitz utility function which shows that very small gains or losses don’t really affect our happiness much at all, called the peanuts effect. In reality it is probably a combination of both reasons combined with the fact that the lottery draw is quite exciting if you’re involved.

Prospect Theory is also not merely confined to textbooks and academic papers, it can be used to effect real change. In order to do this, economists and psychologists have to use what’s known as framing which is the idea that the way information is presented can influence people’s decisions. For example, most pension plans simply take a fixed amount of money from your salary every month. This is seen by most humans as a loss and is generally resented since every month you are poorer by the amount you put towards the pension. However, an alternative pension plan called ‘Save More Tomorrow’ involves signing up for a certain rate (say 20%) but rather than starting to pay immediately, you only pay the 20% on any future salary rises. This means that if you are given a £500 a month pay rise, £100 of it would be set aside for your pension. Here people reframe the loss they experience from a normal pension into a feeling of being “less richer” having gained a smaller amount. The end outcome may be exactly the same financially but very different psychologically, with twice as many people willing to use the ‘Save More Tomorrow’ scheme than a normal pension in experiments.

Photo by Jill Wellington on Pexels.com