In the run-up to last year’s festive period, many stock investors were eagerly anticipating their annual gift from Father Christmas – the Santa Claus rally. This refers to a seasonal upwards trend in the US stock market during the last five trading days in December and the first two in January. According to the Stock Trader’s Almanac, the S&P 500 historically tends to rise by an average of 1.3% during these festive seasons. In fact, such rallies occurred in each of the five years prior to last, as illustrated by Figure 1.

However, two major developments towards the end of 2021 looked like they might jeopardise this rally. First, President Joe Biden nominated Jerome Powell for a second term as the Chairman of the Federal Reserve System (the Fed), which disheartened investors who perceived Powell to favour policies bearish for the stock market. Second, the Fed also announced plans to start winding down its bond-buying stimulus program as well as raising its benchmark federal funds rate to combat rising US inflation. Despite these developments, last year’s rally turned out to be one of the best in years. This, therefore, raises the question: why didn’t Powell’s nomination and the Fed’s newly hawkish stance dampen the Santa rally?

To answer this question, we will proceed in three steps. First, we will establish what drives these rallies. Next, we will explore deeper the aforementioned Fed plans. Finally, we will assess why these plans didn’t negatively affect last year’s Santa rally.

What drives Santa rallies?

Historically, two main factors are thought to fuel them: higher average investor optimism and increasing household disposable income towards the year-end. Let us explore each driver in more detail.

First, higher investor optimism during the festive days of Christmas plays out through the following dynamic. During festivities, institutional activity in the stock market tends to decline as professional traders go on holiday. When these cold, rational players temporarily leave the market, the overall stock-trading volume naturally declines. The resulting thinner market becomes more susceptible to influence by retail investors. These players, in contrast to the professional traders, tend to be driven more by emotion and have a generally bullish attitude towards the market. This dynamic, combined with the overall Christmas merriness, tends to propel stocks higher, thus facilitating a Santa rally.

Second, rising household disposable incomes towards the year-end – often thanks to annual bonuses paid in December – facilitate the rally in the following way. More cash leads to higher expenditures among households. In fact, as Figure 2 shows, they tend to spend about 2% more on average in December than across the other months.

The increased household consumption also benefits the overall economy and consumer-discretionary companies in particular, driving share prices higher. Some of the extra disposable income ends up as direct investment in the stock market, encouraged by the Christmas-fuelled optimism. The ensuing combination of higher consumer spending and a stronger flow of cash into stocks leads to a rising market, thereby supporting a Santa rally.

What plans did the Fed announce?

In December 2021, the Fed announced a new strategy to tighten its monetary policy. This was triggered by the rapidly rising US consumer inflation which was forecast to reach nearly 7% by the end of 2021 as shown by Figure 3.

Such significant price acceleration was driven by three factors. First, the Covid-19 pandemic caused severe disruptions in global supply chains, leading to widespread shortages of both consumer and industrial goods and, inevitably, to higher prices. Second, after a sharp rise in unemployment to nearly 15% at the depth of the pandemic in April 2020, the US job market recovered markedly as illustrated by Figure 4.

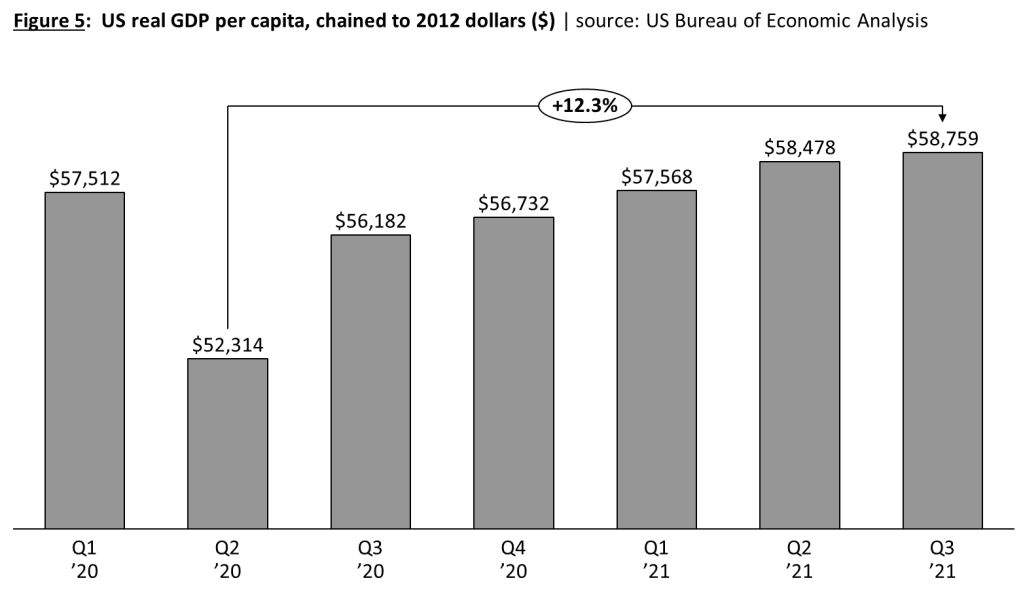

This led to a much tighter job market than anyone had anticipated, with resulting upward pressure on wages. Finally, both the Fed’s and US Treasury’s stimulus programs made more money available to consumers and businesses alike, helping the economy to recover strongly. This is evidenced by the growth of real GDP per capita of over 12% since the second quarter of 2020 as shown by Figure 5.

This trifecta of rising prices, stronger wages and a more robust economy led the Fed to conclude that any further monetary stimulus was not necessary and could be more harmful than beneficial due to the inflationary pressures. In Powell’s own words, “The economy no longer needs increasing amounts of policy support.” Hence, the central bank’s main priority shifted firmly to tackling inflation.

Let us now explore the two main mechanisms comprising the Fed’s expected inflation-busting plan, both aimed at driving higher interest rates for the economy. The first mechanism is more direct and aimed mainly at short-term interest rates: setting a higher level for the Fed’s federal funds rate. This rate serves as one of several benchmarks for the commercial interest rates charged on lending to businesses and households. As the funds rate rises, short-term commercial rates follow, making credit more expensive to companies and consumers. As a result, they invest and consume less respectively, leading to lower demand and moderation in prices for both industrial and consumer goods. The second mechanism is more indirect and aimed chiefly at long-term interest rates – through accelerated tapering of the Fed’s asset-buying program focused on the US government bonds (i.e., Treasuries), which was originally conceived to stimulate the economy by driving down bond yields and injecting more liquidity. A faster tapering of the program is expected to lead to a higher supply of Treasuries in the open market, driving down their prices. Given that a bond’s price and yield have an inverse relationship, this will push Treasury yields higher. Since they serve as key benchmarks for mid to long-term commercial lending, corporate and household borrowing will become more expensive, reducing business investment and private consumption. This is ultimately expected to cool the demand for industrial and consumer goods and, as we determined earlier for the first mechanism, may help temper inflationary pressures.

What was the resulting impact on the Santa rally?

The Fed’s plans described above are consistent with its stated mission of conducting the monetary policy “…in pursuit of maximum employment and stable prices.” So, let us now assess what impact, if any, the central bank’s new policies had on last year’s rally.

Intuitively, one should expect the Fed’s tightening stance to weaken the likelihood of a Santa rally. The causal mechanism underlying this assumption, structured around the two direct drivers of profit – revenues and costs – is as follows. On the revenue side, we should expect a weakened trend, as higher interest rates are likely to dampen demand for both industrial and consumer goods and services, especially discretionary ones. On the cost side, we should equally expect headwinds, because more expensive credit means more spent on debt repayment and less on R&D, eroding future profits. Hence, both sides of the profit equation are likely to be negatively affected by the Fed’s plans, ultimately diluting business margins. Ceteris paribus, this should result in weaker fundamental valuations of publicly traded companies, leading to reductions in share-price targets from financial analysts, and resulting in lower bids by investors.

In reality, however, the Fed’s plans had no dampening effect on last year’s Santa rally. Instead, the S&P 500 index rose by 1.4% – its best showing over the past six years, as evidenced by Figure 6.

Our proposed explanation for the above is that investors merrily assumed that the Fed’s tightening would commence only deep into 2022, without any immediate threat to company valuations. Yet, this managed to only ‘postpone’ an inevitable market reaction, which transpired in earnest in January, plunging all broad US indices down into ‘correction’ territory under the weight of the Fed’s plans. It seems that the joyous rally ride with Father Christmas is likely to be followed by a stiff post-holiday hangover.

Intriguing article – very well written

LikeLike