Over the past 10 years the way we listen to music has been revolutionised by streaming services. Platforms such as Apple Music, Deezer and Soundcloud provide a platform to access almost any song instantly, and a way for artists to distribute their creations without having to press CDs or vinyl. The “headline act” of these is undisputedly the Swedish giant Spotify, which drowns out the competition with 480+ million users, 80 million tracks and a valuation of $30.5 billion – almost double that of its closest rival Apple Music.

Despite popularity with users and its contribution to increasing the accessibility of music distribution, Spotify has sparked controversy over how it pays artists and the potential for this to disproportionately hamper small acts. So, is this accusation justified? If we zoom in on how Spotify has changed the game for stakeholders within the industry: artists and labels acting as suppliers of music, and listeners as the consumers, we discover how Spotify has changed the game.

It is hard to claim that consumers are worse off. Instead of having to venture out to purchase albums or mixtapes, we can now do so through the small handheld device we rely on so heavily. Some claim this ease of access makes the listening experience more passive, losing the connection a vinyl junkie feels with their possessions. However, with 290 million free subscribers, music on Spotify is listened to by the average American for 140 minutes per day across an average of 41 artists per week. This heavily indicates the large demand for music consumption and surely, therefore, providing overall growth to the industry?

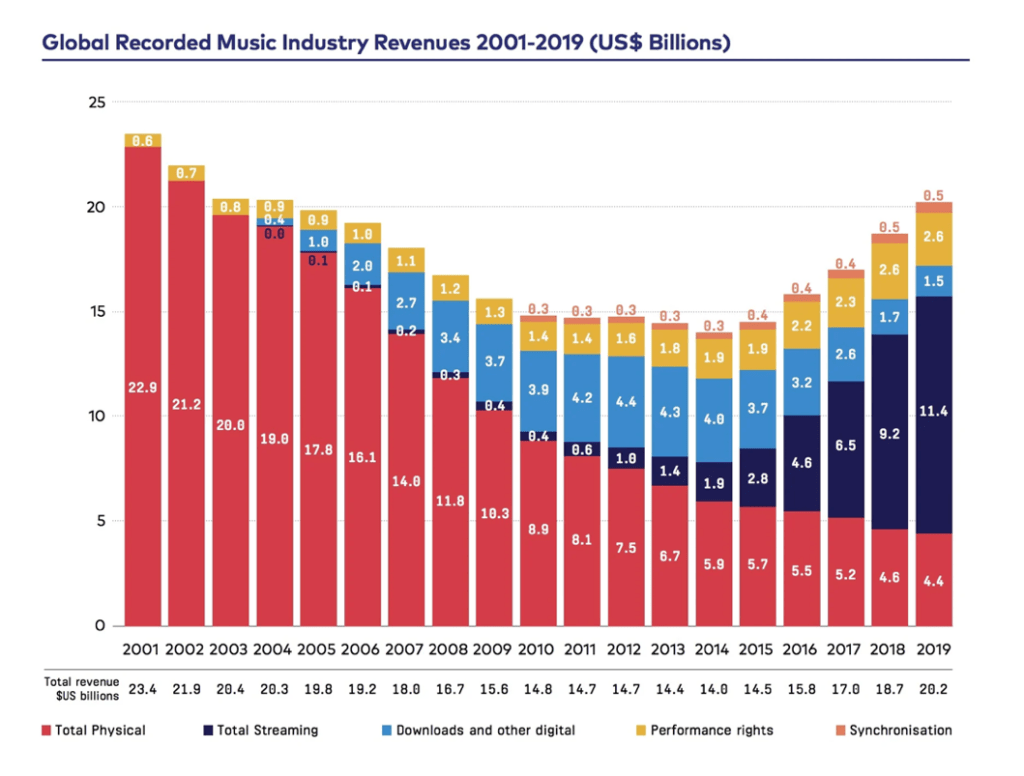

The advent of streaming in the mid 2010s reversed a downward trend in music revenues – a decline caused by a proliferation of illegal and pirated downloads, which Spotify combats efficiently with scrutinous regulation on all songs and podcasts uploaded to the platform. They prevent any sort of unlicensed bootlegs (illegal records) or reuploads from sticking around which, alongside similar platforms sharing alike methods, has helped bring the suffering industry back to life.

As the market leader holding 30.5% of the market for streaming service subscribers, Spotify has played an enormous role in this growth. However, the most contentiously discussed stakeholder in the streaming revolution is the artist. Let’s look at Spotify’s case:

To really understand how Spotify interacts with artists, we must first delve into how they are paid. Each month, Spotify gathers earnings from advertisements and paid “premium” subscriptions (around 42% of listeners.) They then deduct various costs like corporate taxes and credit card processing fees, with the remaining revenue pool consisting of around 65-70% of the original. With this they pay royalties to the rightsholders of the records streamed. Royalties are payments to asset owners for use of copyrighted assets. As is the case with most major streaming platforms, the “streamshare” mechanism is used to determine the precise amounts paid. This method involves rightsholders being paid according to the share of this pool generated by their assets. In most cases, rightsholders refers to the label to which the artist is signed, who own the rights to the recording of the song, and the artist themselves who own the rights to the musical material of the track – the publishing rights. The deal between these two determines the fraction of the royalties passed on to the artist by the label. Spotify plays no part in this arrangement. Thus, there is not a set “per-stream” payment, as is often misinterpreted. The figure often given as Spotify’s average per-stream (APS) payment – $0.003 – $0.005 – is an estimate calculated after the streamshare process noted above has occurred. Hence, it is not possible for the service to simply “pay more per stream.”

By this metric of APS rate, Spotify is one of the less magnanimous platforms at $3.48/1000 streams, making it relatively difficult to earn a substantial income from streams alone on Spotify. Streaming success on the platform rarely translates to any significant financial benefit, this effect being heightened for smaller artists whose streaming numbers are not hitting the hundreds of thousands and making up a notable fraction of the total monthly streams. As an example, Spotify has around 490 million active monthly listeners. We assume they all listen for 140 minutes, correlating to 40 streams if we take 3.5 minutes as the average song duration. Thus, 490 million consumers streaming 40 songs a day for 30 days, we are given 588 billion streams per month, of which an artist getting in the 10000 streams range makes up a slight fraction.

There are, however, advantages to distributing on Spotify beyond royalty payments. Because it provides a platform for artist to connect with so many listeners around the globe, Spotify opens up the opportunity for one’s profile to be raised. The barriers to entry of posting on Spotify are so low due to cheap, subscription based online distribution services which are just a Google search away, and the possibility of publicity and exposure to a huge audience is enticing. Artists can grow their fan base and leverage this to boost numbers at live shows and profit from ancillary revenue channels like merchandise (including CDs and vinyl), being hired for features, or, in the best case, being covered or sampled by another artist. This is hugely valuable as since another artist is using their asset in their own intellectual property (music), they are owed publishing royalties. Every time the cover/sampled song is streamed or performed, a fraction of the revenue makes its way back to the original artist!

The issue with this is the difficultly in ascribing an economic value to this additional private benefit, as we are working with chances. It is inherently tricky to quantify this notion of exposure delivered by the platform – it gives a potential gain as opposed to a guaranteed one. The artist takes on a responsibility to turn this platform into the success which lures them in.

Owing to Spotify’s massive user community, there is certainly an opportunity for money to be made by record labels as all these $3.48/1000 streams add up. Labels – companies that process, distribute and promote the music of artists they sign – typically keep around 85% of incoming payments from streaming services. Even considering the low APS rate, it all adds up from the entire catalogue of artists a label oversees and accumulates over time as streams flood in from multiple assets. For an independent label with few artists, or an artist working alone, the streaming income provides negligible benefit as they only have the very few sources of royalties in the limited records they have released.

One solution Spotify has been exploring is forming deals with independent artists directly, meaning royalties do not have to travel via labels who deduct a weighty slice. This is, in theory, a win-win as it means Spotify can afford to pay out less to these artists, who also earn more overall as the label’s cut is removed completely. Expanding on this, there have even been suggestions of Spotify branching out into a label themselves, eliminating the need for external third parties. However, this is dangerous territory for Spotify for the same reason the deals above occur infrequently: it is extremely damaging to labels, who form an integral part of the supply chain and, vitally, the promotion of new music and thus the industry as a whole. Spotify works closely with big labels, and the success of the two is often linked i.e. Universal Music Group – the dominant record label globally – owns 3.5% of Spotify. These parties must be on good terms for the technology-based music business to function.

The music industry is no stranger to technology-driven shocks. In fact, it has been reshaped multiple times owing to advancements in tech. Monetisation began with vinyl and cassette tapes, moved to CDs, then downloads which lead to where we are now: the age of streaming. Spotify has established itself as a trailblazer in streaming owing to its user-friendliness and low subscription charges. Whether we refer to it as a monopoly or an oligopoly is questionable, but it is nonetheless refreshing to see a vital part of the cultural world not dominated by the tech giant quintet MAMAA (Microsoft, Amazon, Meta, Apple and Alphabet.) However, given its dominance, Spotify must make sure they continue to encourage grassroots music and independent artists to keep creating. As easy as it might be to fall into the trap of promoting and pouring resources into bigger artists, Spotify has managed to hold up so far, with initiatives like its “Loud and Clear” campaign launched in 2021 offering transparency as to how “the money flows” and what they do to promote small artists. If they can continue to foster a variety of music as they continue to boom, they will act as nothing but a blessing for the music business. Although, if they get the balance wrong, it could push newer artists away from music as a career and significantly weaken the industry from the bottom up.