On 24 February 2022, Russia invaded Ukraine in a significant escalation of the Russo-Ukrainian War (which began In 2014); in response, several countries imposed economic sanctions on Russia. The sanctions saw the various countries introduce an oil embargo, financial sanctions and a freeze of Russia’s currency reserves. The purpose of the sanctions was twofold: to put pressure on the war effort and Putin by undermining the economy and to display political opposition. The impacts of these sanctions significantly damaged all economies involved (shown by predictions of a global recession in 2023) and considerable increases in oil prices. Further to this, Russia was excluded from western markets, and the sanctions may potentially cause a slowdown in globalisation as economies adapt their supply chains; this can somewhat protect countries from price spikes caused by external international events such as the Russo-Ukranian conflict. This article examines these impacts with a particular focus on Germany which is heavily dependent upon Russian fuel.

Initial impacts of the embargo and price rise

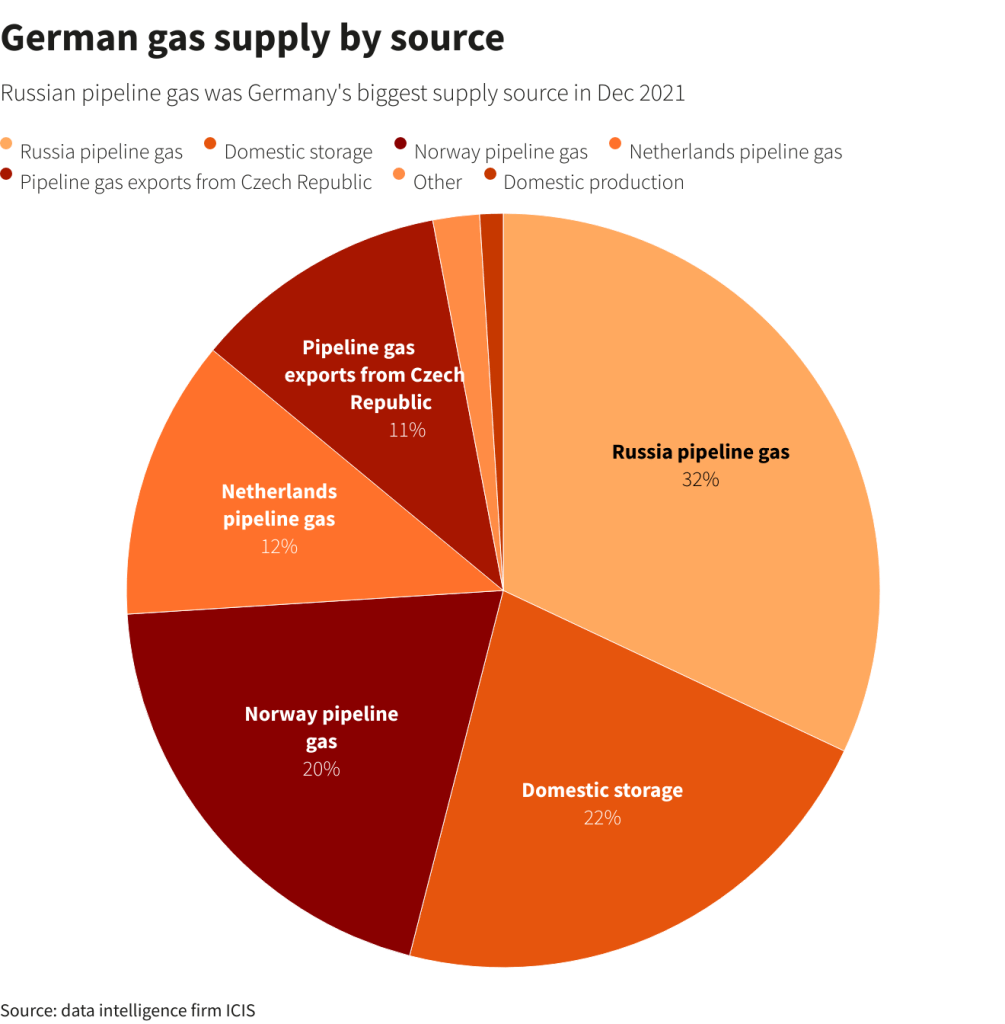

The EU, US, and UK decreased oil imports from Russia to strain the Russian economy and undermine Putin’s war effort. The embargo’s effectiveness is determined by how far prices can be lowered and by a sustained refusal to import from Russia because low prices reduce Russia’s revenue from selling oil. However, initially, the embargo had the reverse intended effect as the invasion of Ukraine saw, initially, the oil market price skyrocket, with oil barrels reaching $105 per unit for the first time since 2014. This consequence damaged both industry and households of countries enforcing the embargo because they are net oil importers. Russia was one of the largest global oil producers, with a 13% market share which accounts for the significant impact of the conflict on the global market price. The European Union pledged to slash 90% of Russian oil imports by the end of 2022, and the US and the UK followed suit. This, coupled with a lack of confidence in the supply chain and lower global supply, further drove up the prices. The high prices prompted cost of living crises, especially in the UK, where energy costs increased quicker than wages. Germany, imported 32% of its natural gas from Russia before the war (see Fig 1), making it particularly exposed to the price rise exacerbated by the sanctions due to its reliance on Russian imports; similar to the UK, the initial damage primarily harmed German consumers. Looking forwards, the effects of the embargo on Germany depend on reliance on Russian imports and the oil market price.

Fig 1: Previous German dependency on Russian imports and thus vulnerability to price rises – ICIS

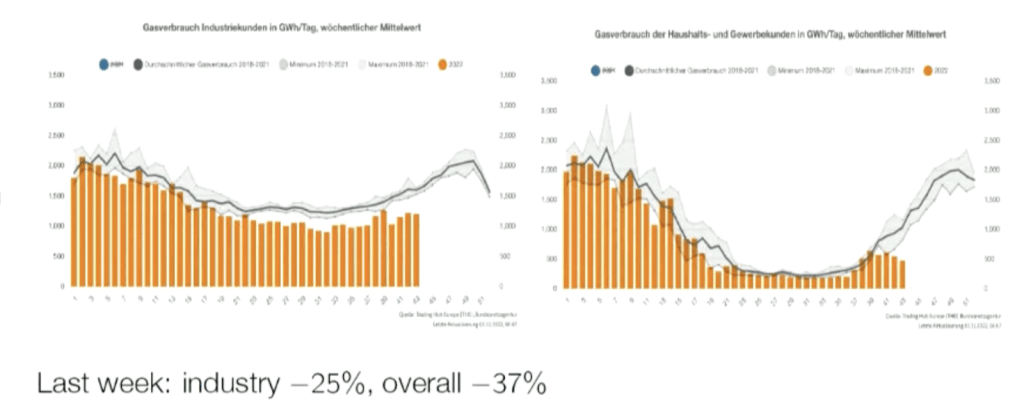

Fig. 2 Large drops in German gas use both industrially (left) and from households (right) (Bundesnetzagentur)

German supply chain adaptation

To counter this initial damage, Germany’s economy successfully adapted to the higher energy prices and reduced gas supply to minimise damage to industrial production and GDP. The supply chain adaptation enabled Germany to survive the winter’s prices and the 37% drop in gas consumption by seeking alternate suppliers and production techniques. The development of less-energy dependant production is an example of dynamic efficiency and has facilitated lower gas consumption. Without adaptation, a cascading effect would be expected to cause a fall in industrial production equal to the decrease in gas usage. However, the 25% reduction in the industrial use of gas resulted in only a 2% drop in industrial production (see Fig 3), showing the extent of German economic adaptation. As expected, there were more significant productivity drops in energy-intensive sectors such as chemical production. This asymmetry demonstrates the adaptation of the German economy to cope with the higher prices and reduced consumption; consequently, the embargo’s self-damaging effects were minimised by eliminating inefficiencies and using new energy sources.

Fig. 3 Only a small drop in Industrial Production – Destatis

New global suppliers

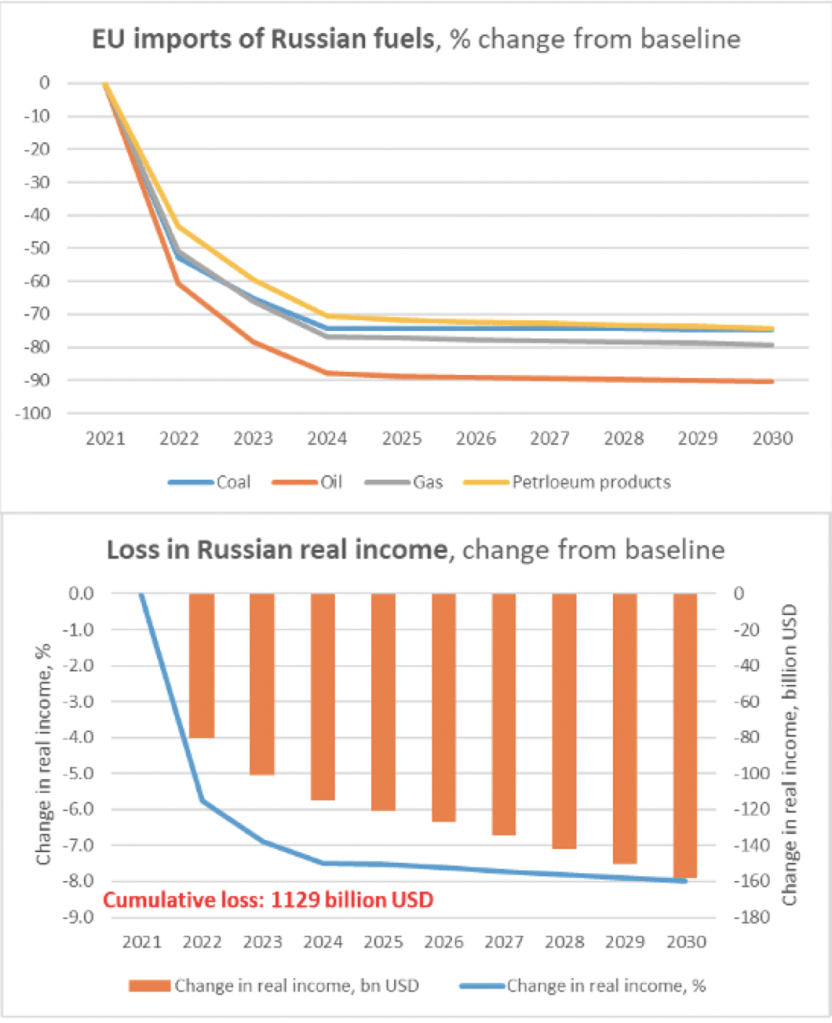

Lower oil and gas prices directly punish Russia as a net hydrocarbon exporter. As intended, Russian exports decreased due to the sanctions (European impacts shown in Fig 4); however, initially, the increased scarcity raised energy prices such that the Russian energy export revenues were 38% higher in 2022 than in 2019. This initial period of backfiring ended after the winter of 2022; prices have since greatly fallen and as substitute suppliers fill the void of Russian oil and gas imports, increasing the global supply, lowering prices and alleviating pressures from the embargo on the enforcers while also degrading Russian export revenues. Through the recent lower prices, Russia is feeling the damage of the embargo and is suffering from lower revenue and real income (shown in Fig 4).

Henceforth the embargo’s effectiveness lies in the speed and scale at which prices can be driven down – influenced by investor confidence as a result of changes in the war as well as other significant hydrocarbon exporters like OPEC. However, the adaptation of supply chains is much quicker with oil than gas because oil is easily transportable, other countries have stored spare capacity, and European infrastructure exists to import non-Russian oil. Russia already has an expensive large-scale infrastructure to export gas to Europe – such as the Yamal–Europe natural gas pipeline. Although, liquified natural gas may facilitate quick alternative supply increases, exporting gas is costly, and the infrastructure takes years to create; therefore, introducing new gas sources to Europe may take longer, meaning prices may fall slower.

Fig. 4 EU imports of Russian fuels and Loss in Russian real income – Centre for Economic Policy Research

Deglobalisation

Another implication of these sanctions is a tendency towards deglobalisation, whereby countries seek more energy security through domestic production instead of importation. As Fig 2 shows, domestic production accounts for only 5% in Germany – which is the case for most European countries. This lack of gas reserves makes these countries extremely dependent upon oil imports and thus vulnerable to sharp price raises caused by external events such as the Russian war and supply shortages. A reduction in globalisation has been observed as governments seek to be more independent and secure, with a rise in support for national, domestic oil production.

The 2008 financial crisis revealed the fragility of an interconnected market caused by globalisation and led to an uptake in protectionism. This inward focus is being mirrored today because of the damage the sanctions are doing to the countries imposing them. Cost of living crises, record-high inflation, and fears of recession amplify economic inequalities, feeding populism and a calling for hardening borders and restructured supply chains for a domestic focus. Such deglobalisation damages trade, though it protects countries from externalities causing price spikes – as seen with Russia.

On the other hand, the pressures of the sanctions may only cause a restructuring of global markets to be more independent of Russia, with supply chains aligned more with geo-political alliances. This is suggested by Germany’s industrial adaptation and economic movement away from reliance on Russia.

Financial Sanctions

Russia’s financial sector has been targeted as the sanctions attempt to damage the rouble and prevent Russian access to global funds and financial systems. The attempts to isolate Russia from global markets saw the country banned from numerous financial systems, including the United Kingdom’s, which prevented Russian borrowing. This harmed Russian GDP and Russia’s potential to expand its capital and is reinforced by how SWIFT is no longer available to numerous Russian banks. This increases the cost of and slows Russia’s financial transactions, harming the sector.

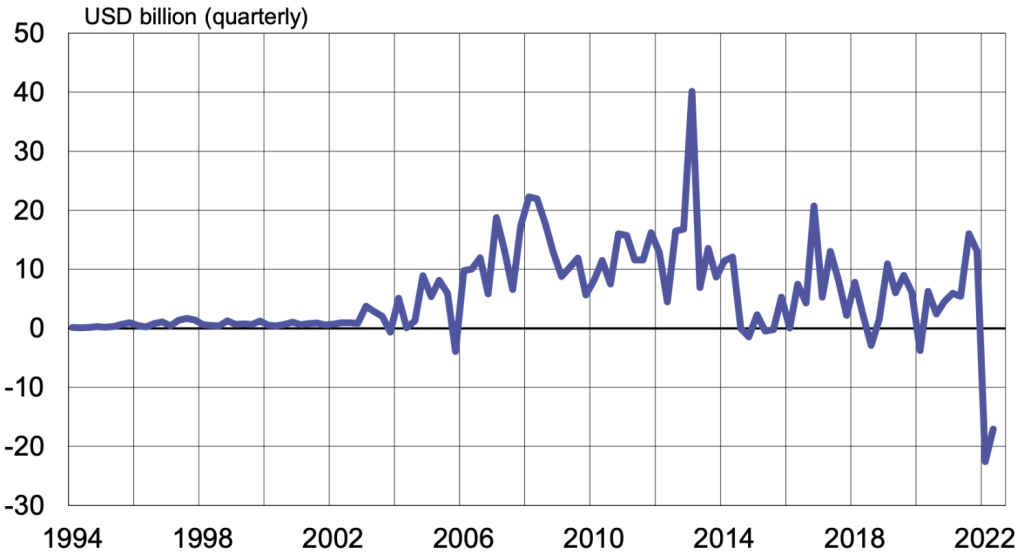

Hundreds of companies have left Russian markets as investor confidence plummeted and political opposition blocked much investment – shown by a trough in FDI (foreign direct investment, Fig 5) – demonstrating a global lack of faith in Russia’s economy and the rouble. These financial sanctions impair Russia’s ability to operate in global markets and have caused significant withdrawals from the economy; Russia is left unable to borrow and finance replacements for their sanctioned imports, further attacking the economy. Being unable to effectively withdraw capital disincentivised investors from Russian investment. As a result, the rouble significantly depreciated, reaching a record low of 135 roubles to the dollar in March. Despite the damage these sanctions have undoubtedly caused, Russian central banks have imposed emergency capital flow restrictions which have limited the damage and calmed Russia’s raging inflation. This measure reduces the impact of these sanctions and sees Russia recover some FDI and experience disinflation to soften the financial hardship.

Fig. 5 – Net flow of inward Foreign Direct Investment to Russia – Centre for Economic Policy Research

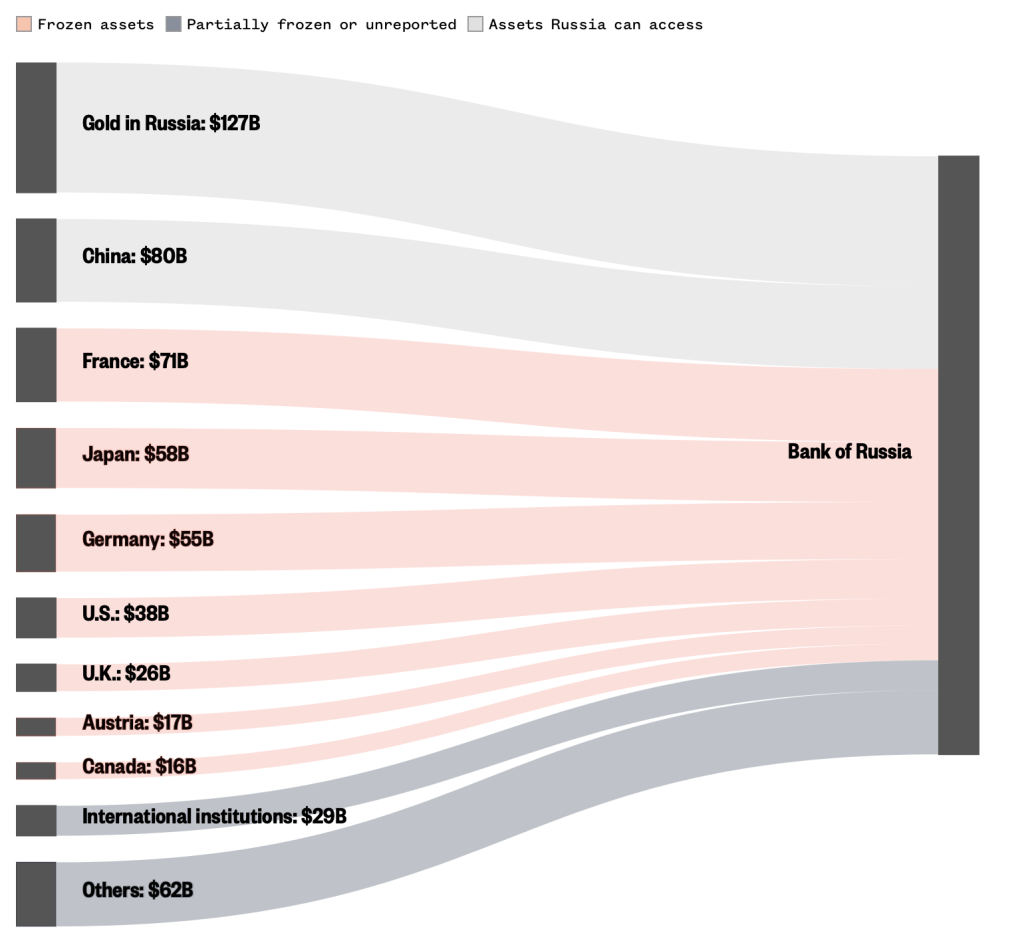

Russian Reserves

Russia holds reserves in commodities and foreign currencies as insurance in case of a depreciating rouble. However, a significant portion of these have been frozen, impairing Russia’s ability to support its economy. The reserves are used to increase support in financial markets and keep a healthy trade balance; they have steadily increased by 75% since 2015. These reserves defend against financial sanctions because they can be liquidated and used to support Russian companies. However, they are primarily frozen, meaning that of the foreign currency reserves, about 50% ($300bn) is not accessible and cannot be liquidated (shown in Fig 6). This sanction leaves Russia vulnerable to other financial sanctions and unable to support its economy suffering from the hardships of the trade sanctions. Russia is currently taking legal action in an attempt to regain access to its reserves. If they remain frozen, however, Russian GDP will suffer more substantial damage from the other financial sanctions without the support of the reserves.

Fig 6 – The state of Russian reserves since the imposition of financial sanctions – Riaz Haq

Limited imports

Imports into Russia have been cut by 28% due to the sanctions damaging Russia’s GDP and balance of trade. These sanctions have left Russia unable to import specific components crucial in its production of various technological and military goods. Russia’s war effort is heavily dependent upon imported components – evidenced by how in 2018, only 50% of Russia’s military-related goods were domestically sourced – which has left Russia unable to produce the military capital desired. The embargo also led to a shortage of microchips and semiconductors which prevented the production of many goods; this also hurt Russian GDP, which dropped by 4.5% in 2022 (a statistic supplied by Russia which is thus potentially understated). The microchip shortage was especially harmful through its damage to the technology sector and military effort because most advanced weaponry, such as missiles, depends upon microchips. This sanction’s continued effectiveness depends on how well Russia replaces the lost imports. China is well positioned politically and economically to fulfil this role of supplier, being Russia’s strongest trade partner. However, China has refrained from this to avoid secondary sanctions. Another determinant of the sanctions’ future success is how well the enforcers can survive the self-inflicted damage of the embargo; high inflation, recessions, and prospects of increased export revenue may see these sanctions therefore loosened. Whilst they remain in place, though, Russia’s output will continue to suffer, and the shortages will damage the technological sophistication of the war effort.

To conclude, the sanctions have implications affecting economies across the globe, including the restructuring of global supply chains. The sanctions have damaged Russia extensively, tanking its GDP and depreciating its currency. Though, this came at a cost, especially in the Winter of 2022, damaging the enforcers’ economies too – plunging various European economies into possible recession. The sanctions’ continued economic and political implications will be determined by how well these policies can be maintained, changes in economic policy from important global influences such as OPEC and China, and how global supply chains will adapt to reinforce Russia’s exclusion from global markets.