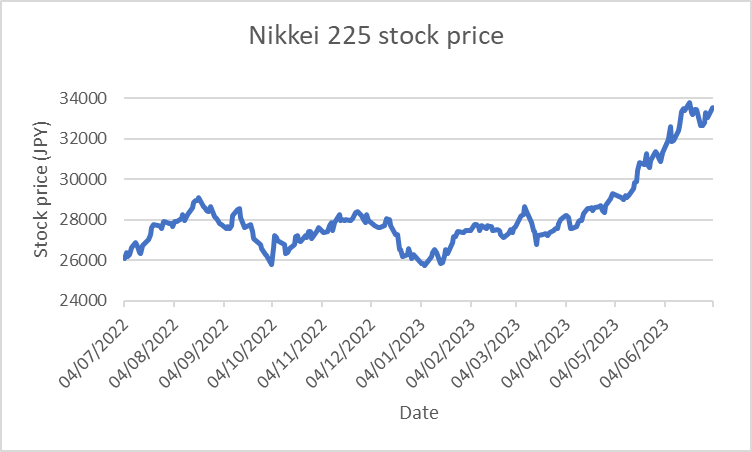

July’s chart of the month shows how Japanese stocks have performed since COVID. In 2023 alone, the Nikkei 225 has grown by 30%, triple that of the S&P 500, and far exceeding the growth of most European indexes. The Nikkei is now only 20% off its peak in 1990, growing 6% in June. Investors must ask: have Japanese stocks at last recovered from a 30-year malaise? Or has the Japanese stock market once again overpromised, as it did in 1990, 2000 and 2007?

In the mid-1980s, the Japanese stock market faced a run of unbroken growth. Between 1985 and 1990, the size of Japan’s economy almost doubled, due to a combination of low interest rates and rapid industrialisation. However, as interest rates rose, frenzied speculation on both the property and stock market was revealed to be unfounded: the Nikkei peaked at 38,000 Japanese yen in 1990, falling to 7,000 in 2009, after the financial crisis. Low growth and poor returns have pervaded: only 50% of profits go back to shareholders, compared to an American average of 80%, and Japan’s GDP has shrunk since 1995.

The simplest explanation for the Nikkei’s rally is the relatively cheap price of the index. Around half of the listed stocks have a price to book ratio of less than 1, meaning the price of a share is less than the equivalent value of the firm’s assets. In comparison, only 3% of US firms on the S&P have the same problem. Corporate earnings are also higher for Japanese stocks, with the price to earnings ratio being 14, compared to a US average of 19. All this suggests that investors can expect high dividends, and higher stock prices, until the disparity is corrected. In June, Warren Buffet, known for his reliance on value betting, upped his stake in Japanese trading houses to 7.4%. If this is truly the explanation for the rally, there may still be space to grow.

However, the Nikkei has been cheaper than the S&P for decades, and yet the index has failed to gather momentum: investors did not see the growth they expected in 1998, 2003 or 2012. Cheap prices alone are not a sufficient explanation for the Nikkei’s strength.

COVID also played a role. Consumer spending increased significantly in 2023, and investors expect that household spending will pick up as Japan opens up. Japan was one of the last countries to reopen after COVID, meaning consumers will look to spend their savings, having missed out over the last few years. This should provide a short term boost to the Japanese economy, and so the Nikkei.

Perhaps the most significant cause for the Nikkei’s growth is Japan’s inflation. Since the mid-1990s, inflation in Japan has been stubbornly low. Shinzo Abe’s programs of government spending on infrastructure, as well as ultra-low interest rates, have failed to increase the country’s rate of inflation. In 2021, Japan once more faced deflation, of -0.24%. Deflation discourages consumers from spending, as they expect prices will go down if they wait; worse, Japanese citizens save 55% of their wealth in low-yield cash deposits, which will not go to

the kinds of risky investment that lead to high growth. If inflation can encourage citizens to finally increase spending, wages could increase alongside prices, triggering a positive feedback loop, and a return to high growth. So far, wages have only risen 1%, below an inflation rate of 3%; but if inflation is long term, then growth may be around the corner. Inflation has the inverse effect, encouraging consumers to spend to avoid high prices.

However, inflation in Japan is primarily caused by short term supply side factors. high import prices due to damaged supply lines over COVID, as well as the Russia-Ukraine war have pushed prices up in Japan, as worldwide. But when these subside, Japan may see a return to low inflation. Japan’s 3.2% inflation rate may be temporary, and some investors are wary of predicting long term wage growth.

Thirdly, global conditions have been a source of growth in recent months. While Europe faces high interest rates, and the risk of recession, China has faced a disappointing economic recovery coming out of COVID. Japan on the other hand has been able to maintain low interest rates, due to its relatively low levels of inflation, 5.5% lower than in Europe. Interest rates have further served to boost exports by lowering the prices of Japanese goods internationally, leading to surging profits, as Japan runs a current account surplus (exports exceed imports). Due to weakness in Europe and in Asia, investors seeking high returns may invest in the Japanese stock market, as their next best option.

Lastly, there are signs of change in the fundamental conditions that have brought low shareholder returns and low growth in Japan for decades. In particular, Japanese firms have a history of sitting on large amounts of cash, and appear resistive to the interventions of foreign investors. Take Cosmo Energy Holdings, where activist investor Yoshiaki Murakami’s attempts to spin off Cosmo’s renewable energy business were met with a poison pill, that took away Murakami’s voting rights. This traditionalism has disincentivized foreign investors, and led to lower growth across the economy.

Now, the government intervention that was once a cornerstone of Shinzo Abe’s three arrows may be having an effect. The Tokyo stock exchange has advised firms with a price-to-book ratio of less than one to increase their share price, but they haven’t taken direct measures; nonetheless, firms have been responsive. Share buybacks in Japan totalled $6.2 billion thus far in 2023 – this not only pushes up the share price, which should enable firms to raise additional cash, but injects stagnant cash back into the economy. Additionally, activist investors appear to have been given a little more leeway – canon shareholders successfully reprimanded their CEO for failing to appoint more female directors. These are signs of structural change, which may mean more growth in years to come.

Whether these moves are the sign of a new outlook for Japan, with stronger growth, higher spending among households and increased competitiveness among firms, remains to be seen. However, the significance of decades of culture should not be underestimated. It may take a little more than guidance from the Tokyo Stock Exchange for firms to pay out substantially higher dividends, or to push up stock prices for good. Equally, for Japanese consumers to start buying shares instead of bonds may take more than six months of positive growth. Certainly, monetary policy, government regulation, and international conditions will all play a role in the uncertain future of the Japanese stock market.

Our Question of the Month:

Is the growth in the Nikkei-225 reflective of long-term growth in Japan, or short-term pressures?

Written by Thomas Potter