Since the foundation of the Grameen Bank by Muhammad Yunus in 1983, microfinance, the provision of banking services, and particularly collateral-free lending services, to the poor in developing countries, has been seen by many as a way to unlock the economic potential of the estimated 2.5 billion financially excluded adults in the world (Sultan & Masih, 2016). This access to credit for the almost 80% of those living on under $2 per day (Ibid.) was seen not only as a way of turning entrepreneurial spirit into rapid economic growth, but also as panacea for world poverty. Although the microfinance institutions (MFIs) provide favourable anecdotal evidence, empirical studies of the effects of microfinance have been limited and have returned mixed results. An evaluation of the potential of microfinance, however, shows it to be a key part of the growth and maturing of developing economies, but not by itself the revolutionary engine for growth promised.

Microfinance is a driver of economic growth as it allows the severely poor to escape from poverty traps and therefore produce meaningful amounts, contributing to GDP, instead of negligible figures.

Figure 1 shows the S-shaped curve of a poverty trap, which holds true in many situations across the globe. Below Y*, a family’s income will not be sufficient to make the necessary short-term investments, for example in food to eat or fertiliser on a farm, needed to increase their income in the next month or growing season. However, if it is above Y*, then the family will be able to increase their income year-on-year, due to small investments paying off, but requiring a minimum initial investment. A small, short-term loan can push a family’s income above Y*, setting in motion this virtuous cycle and increasing per capita incomes, one definition of GDP growth. Before microfinance, the only way for families to obtain the cash needed to get themselves above Y* was through informal moneylenders, who, due to the lack of competition and the administrative costs of lending that do not scale with loan size, charged annual interest rates of around 40-200% (Duflo & Banerjee, 2011), meaning that the interest costs could drag future income back under Y*, leaving the family stuck in the poverty trap. Microfinance, through its rigid, group-orientated structure, managed to bring the costs of lending down significantly, and introduced competition to the lending markets, resulting in interest rates as low as 20% per year (Ibid.), allowing the families to move out of the trap and increase their incomes.

However, the one thing the MFIs cannot control is the willingness of the locals to take out loans with them. The rigid structure of the loans and the focus on zero-default, the aspects of microfinance that allow it to offer such comparatively low interest rates, deter many from using the MFIs in the first place. Evidence from randomised controlled trials (RCTs) in Hyderabad show that the introduction of MFIs into poor neighbourhoods only led to one quarter of all families borrowing from them, while leaving the fraction borrowing from informal moneylenders, at much higher rates, unchanged at over one half (Banerjee, et al., 2009). The repayment of MFI loans typically starts a week after the loan is given out, with exceptions only being made for medical emergencies. This deters anyone who is planning a project which will reap long-term rewards from taking out a microfinance loan, or anyone who holds any uncertainty about their ability to immediately repay the loan. The repayment also happens in groups, and this requirement of joint liability means that social pressure is put on all in these groups to play it safe and not take risks (Duflo & Banerjee, 2011), discouraging those taking on risky projects from taking out a microfinance loan. Furthermore, for poor people trying to run their own businesses, the time costs imposed by having to meet weekly to discuss their loans and repay them might be too much for them. In this way the structure of microfinance loans imposes a limit on the number of people that they can reach, and therefore the potential growth that can be unlocked.

This also exposes a structural flaw with the MFIs. The collective responsibility and localised nature of the MFIs means that the social equilibrium on which the loans are based is only stable up until a point (Ibid.), and a political shock to this social equilibrium can therefore spell the end of microfinance in an area. This can be simplified into game shown in fig. 2, involving the clients of an MFI, all with loans of ₹10,000[1], total interest payments of ₹1,000, and the ability to generate ₹2,000 extra income with their respective loans. All clients either have the option to repay their loan (R) or default on it (D).

There are two pure-strategy Nash equilibria in this game of strategic complements: the single client along with all other clients repaying their loans, in which case the MFI survives; and all clients defaulting, in which case no-one has to repay anything and microfinance is eliminated from the area. As long as the single client believes that more than 92.3% of the other clients are going to repay their loans, then R is their best response. However, as soon as this percentage drops below this figure, D becomes the best response for all involved, leading to the bankruptcy of the MFI (this is more applicable for MFIs than for any banks, since MFIs have localised lending schemes and rely heavily on microcredit, instead of other financial services). Even when played out as a realistic repeated game, the benefit of the income from defaulting is far greater than the repeated benefit of loans, and so the outcome is similar. This means that the ability of an MFI to drive growth in an area in the long term is dependent on the often highly volatile political behaviour in that area, as shocks such as the government-driven ‘Movimiento No Pago’ in Nicaragua (Minchew, 2011), or the promise of a law in 2010 in Andhra Pradesh allowing the non-payment of MFI loans for farmers (Bhandari & Kundu, 2013), can be enough to push people into believing that the percentage repaying will be below 92.3%, leading to the Pareto dominant, but socially suboptimal, equilibrium of everyone defaulting, and therefore making MFIs too fundamentally insecure to be a truly revolutionary engine for growth.

It can be argued that microfinance promotes growth as it develops and deepens the financial sector, making credit markets thicker, faster, and more accessible, a process which is central to the development of small businesses and economic growth. MFIs increase demand for bank loans, since they provide their clients with a credit history and with increased incomes and assets, as shown earlier, making those clients more likely to qualify for bank loans, either with a bank or with a bank partnered with an MFI. This increased demand leads to the development of the banking system as it will encourage it to cover more of society and to enforce its regulations over a greater share of lending activity (Tressel, 2001). This results in growth as it leads to the more efficient mobilisation of savings and allocation of capital, as well as reduced costs of borrowing due to the economies of scale employed when collecting information and spreading risk, such that more and more firms are able to borrow, invest, and increase their output.

Furthermore, formal financial sectors are key to growth as they channel savings to innovative entrepreneurs (Schumpeter, 1955), and so by extending formal lending services to the estimated 2.5 billion financially excluded adults in the world, many microbusinesses will be able to scale themselves up by investing in new capital goods, labour, and inputs, allowing them to produce more, and causing GDP growth. Microfinance can position itself as the intermediary between the formal and informal lending sectors, providing the knowledge and security that the informal moneylenders have while also being able to raise the credit that the formal banks have access to (Barr, 2005). Therefore the many firms which have the potential to grow or have innovative ideas, but are held back by either their lack of assets or the small initial loan size that they want, are able to unlock this potential for growth through microfinance’s provision of credit.

However, these businesses are destined to never grow substantially, and so microfinance by itself can only ever have a limited impact on growth (Duflo & Banerjee, 2011). Due to the small-scale nature of the businesses that the poor run, and the fact that most are undifferentiated from those around them, although the marginal return on investments is high, the overall return is still very small, and the return on the investment is subject to large decreasing marginal returns (curve OP on fig.3), as evidence from RCTs has shown (de Mel, et al., 2008). In order for these microenterprises to scale up to a reasonable size, they need to have an idea that differentiates them from the others (i.e. not another t-shirt stall), and need to make further investments in labour and capital machinery (the productive potential of which are shown by QR) that, for most people, are way beyond what they are able to do. A loan of OQ is far beyond what any MFI is willing to give out and beyond what risk it is willing to take, yet the assets of a business of such size would be too small to be collateral for a conventional bank loan. Furthermore, switching from OP to QR may require some management and other skills that the entrepreneurs, for the most part, either don’t have or can’t afford (Duflo & Banerjee, 2011). This inability to scale businesses with constant returns on capital invested, and the inability of banks in developing countries to provide risky loans to allow small, but not tiny, businesses to grow into medium-sized regional businesses, largely explains why RCTs showed no change in the number of people that businesses employ, a rough proxy for business size, when local MFI branches were introduced to increase the provision of microcredit in Hyderabad, with only 10% of all businesses employing non-family members (Banerjee, et al., 2009). The upper bound set on the size of the businesses therefore sets an upper bound on just how much microfinance can cause growth.

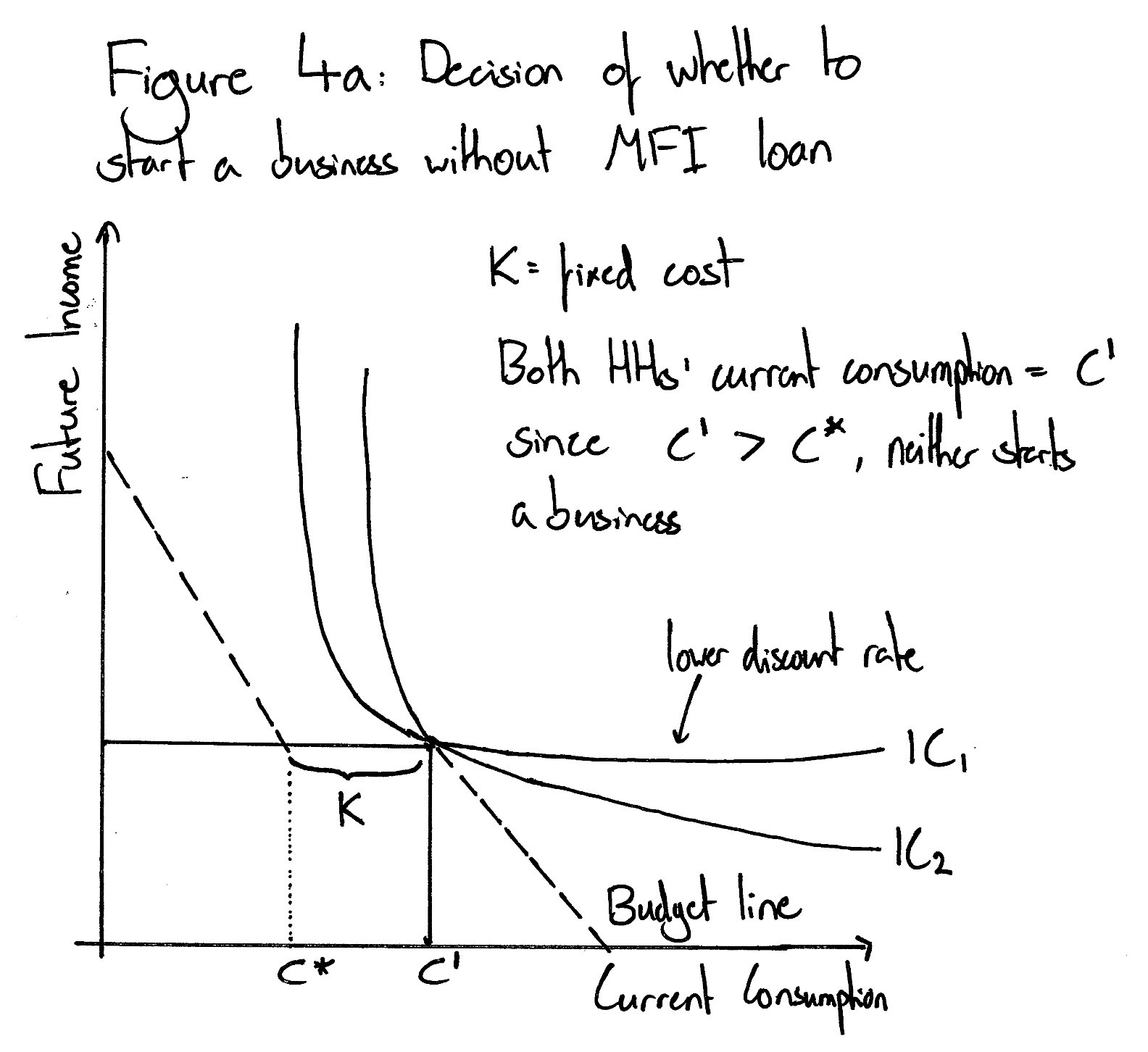

The fixed costs of starting a business also lead to minor differences between families and situations deciding whether a microfinance loan is used to start a business, hopefully leading to sustainable growth, or whether the loan is just used to increase current consumption (Banerjee, et al., 2009). Fig. 4 (Ibid.) shows how slight differences in the discount rates of two families with the same initial income can lead to these different decisions when MFI loans become available: the loan becoming available reduces the reduction in current consumption needed for an increase in future income, shown by the shift in the budget line, causing both families to take out the loan, but the family with IC1 uses it for starting a business while the family with IC2 uses it to increase current consumption, due to the fixed cost of starting a business making the budget line non-linear. Since such small differences dictate decisions of whether or not to start a business, microfinance cannot be a truly revolutionary engine of growth unless most poor families in developing countries are not even slightly myopic.

Unfortunately, due to the psychological aspects of life in developing countries, those taking on MFI loans tend to be myopic. There is a strong positive correlation between poverty and the stress hormone cortisol, which has been found to negatively affect areas of the brain such as the prefrontal cortex, meant to inhibit impulsive decision making, therefore raising the discount rates and reducing the ability of those under these conditions to make economically rational decisions (Haushofer, et al., 2012). This decreases the likelihood that an MFI loan will drive sustainable growth through the creation of a business, explaining disappointing results such as those from Banerjee, et al. (2009) in Hyderabad, which showed that an 8.3 percentage point increase in the likelihood of having an MFI loan only resulted in a 1.7pp increase in the likelihood of having opened a business in the previous year.

There is a case to be made for microfinance as being a tool for development, which in the long run should lead to greater growth. As of 2013, the total number of MFI clients was 211 million, of whom 158 million were women (Microcredit Summit Campaign, 2015), most in countries where women would usually not have much of a say in the financial decisions of families. By giving the loan directly to the women, more of either the income generated from their business or the money from the loan itself would be spent on goods and services which matter to development, such as education and healthcare, since, as the theory goes, the women care more about this side of family life than the men. With increased spending on these, the workforce would become healthier and better educated, increasing the potential capacity of an economy and leading to more sophisticated, higher value-added businesses, causing growth in the long run. This has led to results such as Foccas clients in Uganda spending a third more than non-clients on their children’s education (CGAP, 2002); but since the effects on growth are long-term, there is not much evidence yet for how development driven by MFIs impacts upon it.

Despite these individual results, however, much of the empirical data has shown MFIs to actually negatively impact upon such long-term investment in human capital. Banerjee, et al. (2009) found no statistically significant effect of MFI loans on health and education spending; Islam & Choe (2009) and Maldonadoa & González-Vega (2008) found microfinance to negatively impact this spending. This is because the time constraints imposed on the families taking out the loan by the strict repayment schedule and structure increases the opportunity cost of sending their children to school instead of having their children work for their business, and so while the family has an active loan, they are more likely to at least delay the education of their children, if not abandon it (Emerson & McGough, 2010). Furthermore, the option of saving that MFIs offer, albeit with low interest rates, imposes an extra opportunity cost on consumption of goods with no immediate return such as schooling. The extent of these effects depends on just how poor these families are, as the poorer they are, the more likely they are to want to increase current consumption at the expense of their children’s future income (until their basic current needs are satisfied), and so once again the extent to which microfinance can promote growth depends the extent to which discount rates vary from family to family.

In conclusion, microfinance is not, by itself, the revolutionary engine for growth in developing countries that it was once promised to be. Despite extending the reach of credit markets and giving the poor in developing countries a way to lift themselves out of a poverty trap, in order for substantial, sustainable growth to be driven, other institutions would be required to work in tandem with MFIs, such as ones for financing medium-sized businesses. Therefore, until these extra components are created, microfinance’s impact on growth is limited to what it can do to raise the incomes of the poor, which itself has a ceiling. However, the networks which it is building amidst poor communities, and the information it is gathering on those who never previously would have had formal records, shows promise for the future provision of extra services, such as crop insurance, which themselves could do much to contribute to growth in developing countries.

One thought on “Is microfinance a revolutionary engine for growth in developing countries?”