The COVID-19 outbreak is having a severe impact on the global economy. China had its slowest year of economic growth last year off the back of the trade war with the United States. The timing of the virus could not have been worse, slowing China’s economy even further with their quarterly growth rate dropping to negative 6.8% from 6% in the previous quarter, seeing the lowest rate on record. The UK has also had its problems, stemming from supply chain disruptions due to China’s early shutdown and its business closures resulting in a rise in unemployment and a fall in consumer spending.

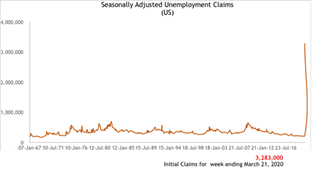

Governments across the world have had to quickly respond to limit the economic damage the virus can cause. On the 23rd March, the UK government announced that non-essential businesses were to close and that there was to be a strict nationwide lockdown. Experts predict that the UK’s economic output will be cut by 15% in the second quarter with unemployment almost doubling. The government reacted with the announcement of the furlough scheme, where workers, unable to be supported by their company, will be paid up to 80% of their income by the government. The aims of this were mainly to reduce unemployment and to keep businesses alive by supporting workers and trying to reduce economic uncertainty. With this support and the increasing number of people looking to claim Jobseeker’s allowance, as seen in the diagram above, the government’s budget deficit is going to increase significantly due to the fall in tax revenue and increase in government spending. The announcement of the scheme to aid employers in retaining employees could cost the UK government upwards of £50 billion with the more prolonged the lockdown is, the more the government having to take on debt.

The graph above shows the unemployment claims in the US alone, spiking as a result of the virus. The figure includes some of the biggest financial crises in history, including the 2008 financial crash, the dot-com bubble, Black Monday and many more. However, none of these significant events can be compared to the impact COVID-19 has had on unemployment claims. It could be argued that COVID-19 has hit the United States hardest with the head of St. Louis Fed predicting a 30% unemployment rate and a halving of the GDP by the summer. With each state having different rules, it’s hard to say precisely when the country as a whole will overcome the virus. This is a big issue for the government as they cannot allow businesses to fully function without risking a second spike in cases leading to a second lockdown which would be detrimental to the economy. One of the most notable states, New York, has been affected most, raising concerns as it contributes to the national GDP significantly with experts estimating a loss of $10 billion to $15 billion in revenue due to a lack in consumer spending. However, the United States’ government has responded to this disaster in various ways. The announced $2.2 trillion coronavirus rescue package is the largest in US history. It includes around $510 billion in loans for large businesses, $377 billion in loans for small businesses, $280 billion tax cuts for all firms and much more. Another major part of the package is the $1200 stimulus payment that was made to the majority of American households (income of less than $75,000 per person) with an extra $500 per child under the age of 17. I expect that this will result in an increase in the wealth effect and consumer spending especially for households on low-fixed incomes.

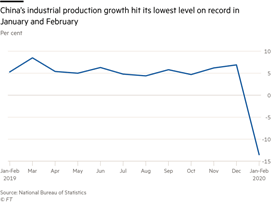

With the original epicentre of the virus being in China, the world’s supply chains were massively disrupted as 30% of global manufacturing is done in China whose factories had suspended operations. Many countries had not been affected by COVID-19 at this point, and so many sectors saw a lack of supply with the usual quantity of goods still demanded, leading to an increase in the average price level. However, China saw its lowest production growth rate on record with it shrinking by 15% from January to February as the entirety of the country went into lockdown, decreasing consumer spending rapidly as confidence was low. China’s unemployment rate increased to 6.2%, which is also the highest rate on record, leaving many without income, further negatively affecting the Chinese economy, lowering both output and consumer expenditure. Retail sales have fallen by around 20% in China, and they expect to recover slowly over the year, although they released vouchers nationwide to encourage spending. The government are also planning to take further fiscal and monetary measures, including easing tax rates, increasing government spending and lowering borrowing costs. They are also trying to meet the extra supply by spending billions of dollars since February. However, experts do not expect China to come out with as big a support package as they launched in 2008 amidst the financial crisis as they are not capable of doing so due to its already exceedingly high levels of debt.

To summarize, with many countries’ economies disrupted by China’s initial lockdown, most have shrunk considerably. The main objective for the majority of governments is to increase consumer confidence so that spending can get back to original levels. However, the uncertainty as to when these conditions will be lifted has also left many businesses in the dark as to when they can start to plan to function, further delaying any future growth. It seems that the longer the global lockdowns continue, the more economies are affected in the long run, with the fear of a second spike not allowing any early easing of the restrictions.