“Now this is not the end. It is not even the beginning of the end. But it is perhaps the end of the beginning”. These famous words delivered by Winston Churchill after the defeat of the Germans at Alamein in 1942, marked a turning point in WWII. Such words would be apt today in the “world war” against COVID-19. The first phase of the shock is ending. The world’s largest economies appear to be past peak new infection levels. Phase two will involve a slow release of the lockdown and the maintenance of some social restrictions. Phase three will be when we have a vaccine and will be when the questions of how the pandemic changed the world will get answered.

What we know already however, is that the “Virus Crisis” is different from any other recent crisis. The Great Recession of 2008-2009, was a financial crisis, where the dramatic weakening of the banking system led to a contraction in available broad money supply and in turn aggregate demand. The 1981 – 1982 recession had some similar characteristics to the Great Recession, with a substantial drop in the money supply, but where this was the direct result of policies to raise interest rates in order to bring the prevailing high levels of inflation under control. The 1973 – 1975 recession was primarily the result of a massive increase in oil prices. This supply-side shock created the dangerous combination of stagnant growth and rapid inflation, known as stagflation.

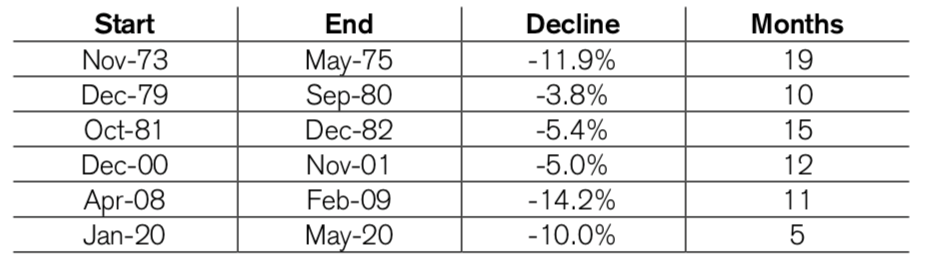

The “Virus Crisis” started as a supply-side shock as production chains relying on goods from China and Asia were halted under the early lockdowns in those regions. As lockdowns began to be imposed on western economies to control the health emergency, an additional demand side shock combined with the supply side shock, resulting in the precipitous collapse in both industrial production and household consumption. As table A below highlights, this twin shock has resulted in the fastest decline in global industrial production ever recorded.

TABLE A: HISTORICAL SHARP DECLINES IN GLOBAL INDUSTRIAL PRODUCTION

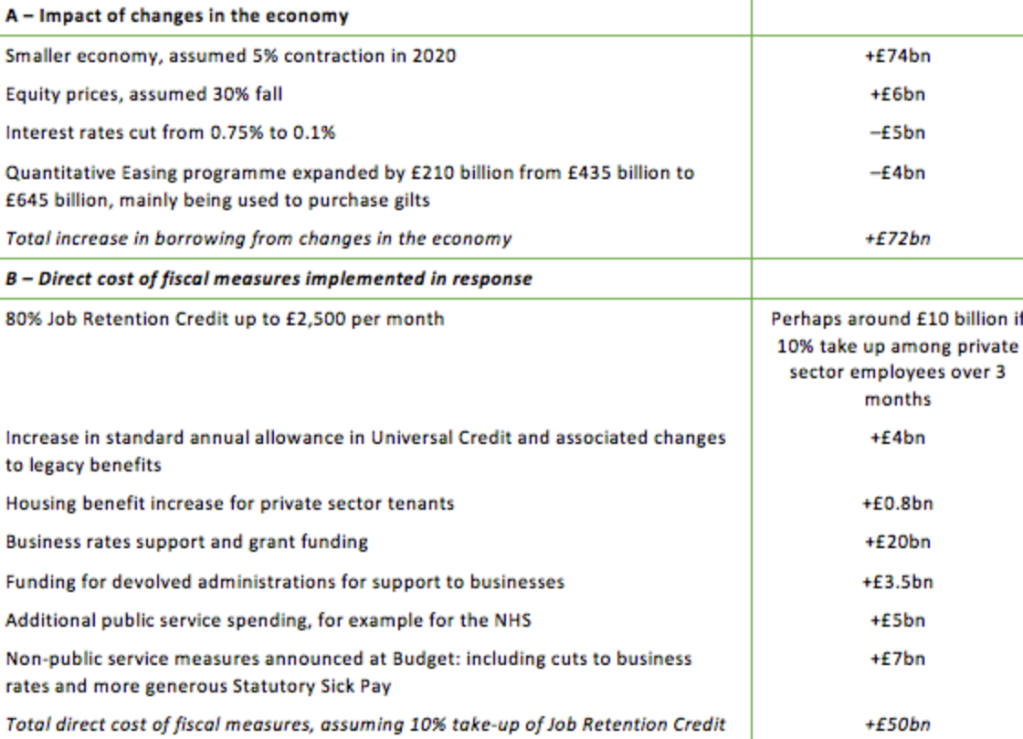

The policy response to fix the Financial Crisis was to provide emergency surgery to the banks to enable them to finance the economy and stimulate demand. This was delivered through a programme of quantitative easing and the lowering of interest rates. It was in essence a monetary solution. The policy response to COVID-19 has not been to stimulate demand but the opposite – to lock the economy down. This has required an extraordinary intervention by governments to keep the payments system going and to prevent widespread bankruptcies and unemployment. The response has been on a massive scale, reaching out directly to businesses and individuals. It has been in essence mainly a fiscal response.

In the U.K., Chancellor Rishi Sunak, has announced a number of direct fiscal giveaways. As Table B below highlights, these include substantial amounts of support for businesses through cuts to business rates and retention credit for furloughed employees (cost: estimated £20bn). In addition, the government has implemented a substantial expansion of social benefits to support those who lose their jobs (cost: estimated £4bn) and additional funding has been made available for public services, especially the NHS (cost: estimated £5bn). In total the estimated cost of these direct fiscal measures is £50bn. In addition, the rapid slowdown in the U.K. economy is expected to add another £72bn to annual borrowings.

TABLE B: IMPACT OF ECONOMIC RESPONSE TO COVID-19 ON BORRWOING IN 2020-21:

To put all this into context, before the pandemic, the Office for Budget Responsibility forecasted the U.K. budget deficit to be £55bn for this current fiscal year. The cost of the impact and policy response to COVID-19 is estimated to add another £122bn, tripling the deficit to £177bn.

How will this be financed? The Government will have to substantially increase its borrowing programme, but from whom? On the 9th April, the Government made an important announcement that it would extend the size of its bank account with the Bank of England (the “Ways and Means Facility”) from £370m to an unlimited amount. As the Financial Times put it, rather than rely solely on the bond markets,

…the UK has become the first country to embrace the monetary financing of government to fund the immediate cost of fighting coronavirus, with the Bank of England agreeing to a Treasury demand to directly finance the state’s spending needs…

So, in summary, the response to COVID-19, has led to (i) the removal of any budget rule constraining the government from spending more than it receives in taxes (ii) the prioritisation of fiscal policy to ensure the economy operates as close to its productive capacity as possible and (iii) an arrangement with the central bank to fund the some of the costs of the policy response by effectively “printing money”.

Put another way, the U.K. government has adopted the central principals proposed by the Modern Monetary Theorists. The MMT genie is indeed out of the bottle.

But does this matter? According to Stephanie Skelton, economic adviser to Bernie Sanders and ardent supporter of MMT, “COVID-19 will lead to massive budget deficits, but this will be fine”. As long as a country can borrow in its own currency, then the level of government spending should not be limited by how much it can raise in taxes. A deficit of the government can be viewed as a credit elsewhere in the economy such that fiscal policy should be activated to provide sufficient credit to ensure full employment. Not surprisingly this “economic theory” has been adopted by politicians on the “far left” in order to provide economic underpinning for their policies on guaranteed jobs, universal healthcare and the Green New Deal.

But the real answer is that letting the MMT genie out of the bottle does matter. Large scale public sector investment risks crowding out private sector investment (through higher taxes, higher interest rates and reduced available savings). Exchange rate devaluations are likely to arise and create trade tensions with countries who don’t have control over their own currencies. But probably most importantly of all, the hyper use of fiscal policy would put aggregate demand management and control of inflation back into political hands. With populism on the rise, the temptation to resort to the printing presses to fund government “pet projects” may prove too irresistible for the MMT genie to be put back in the bottle. It is worth remembering that quantitative easing, the central policy response to the Financial Crisis, was supposed to be a temporary measure but remains in use over a decade later!

Skelton does a thorough job of explaining why “crowding out” can not and does not exist. The notion of crowding out is based on the false assumption that the gov is simply another competitor in the market to borrow money. It is not. The gov is unique in that it issues its own sovereign currency and can provide deficit funding without regard to having to compete in credit markets.

LikeLike

A message to the author: fantastic read, informative text in harmony with interesting statistics.

LikeLiked by 1 person

Hugely appreciated. Any additional thoughts on “crowding out”?

LikeLiked by 1 person